This article is for Irish company directors, business owners, and finance managers who need to understand their legal obligations around keeping company records.

If you're unsure how long to keep invoices, board minutes, employee files, or tax records—or worried about what happens if you get it wrong—this guide covers the exact retention periods required by Irish law, what records must be kept permanently, and the real consequences of non-compliance.

Key Takeaways

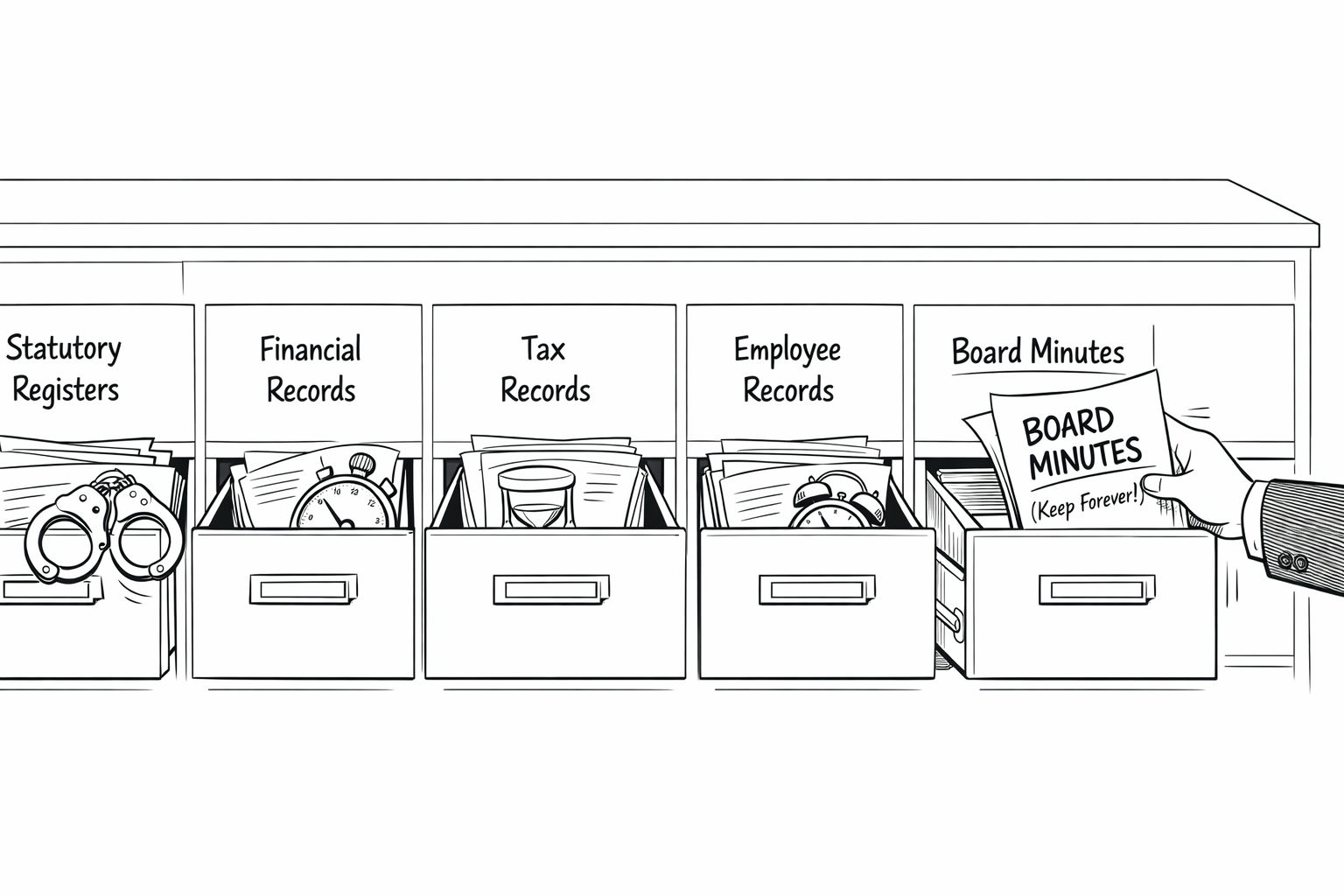

• Statutory books including registers of members, directors, and beneficial ownership must be maintained permanently throughout the company's life.

• Keep all financial records for a minimum of six years, though nine years is widely recommended for protection.

• Board minutes and resolutions are permanent records with no expiry date and must be preserved indefinitely.

• Employee records must be kept for six years after employment ends to cover breach of contract claims.

• Failing to maintain proper accounting records is a criminal offence, and directors can be held personally liable.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

How long do I need to keep my company's financial records?

You must keep financial records for a minimum of six years after the end of the financial year they relate to under the Companies Act 2014. However, nine years is widely recommended in practice because Revenue audits can look back six years, and where fraud or serious error is suspected, that window can extend further back.

Do I need to keep board minutes and resolutions forever?

Yes, board minutes and resolutions are permanent records with no expiry date. You must preserve every written resolution, board decision, and general meeting minute for as long as the company exists, and for six years after it is wound down.

Can I delete old work emails to free up storage space?

No, not if they relate to company business. Emails containing board decisions, contract agreements, or financial information fall under the same retention rules as any other document of that type. Financial emails must be retained for a minimum of six years, and emails documenting board decisions should be retained permanently.

What happens if I can't produce records during a Revenue audit?

Missing records significantly weaken your position in Revenue audits. Revenue can apply estimated assessments, and the burden of disproving them falls on your company. In litigation, courts draw negative inferences from missing records that should have been retained.

How long must I keep employee records after someone leaves the company?

It depends on the type of record. Employment contracts and related documents should be kept for at least six years after the employment ends due to the Statute of Limitations for breach of contract claims. Working hours and payroll records must be kept for a minimum of three years, though six years is recommended for payslips.

Does GDPR mean I have to delete personal data after a certain time?

GDPR creates a two-sided obligation: you must keep records long enough to satisfy statutory minimums, but you must not keep personal data indefinitely once those minimums have passed. GDPR does not override statutory retention requirements like the six-year rule for financial records.

What are statutory books and do they expire?

Statutory books are permanent records that must be maintained throughout the life of the company, including the Register of Members, Register of Directors and Secretaries, Register of Beneficial Ownership, Register of Share Transfers, and Register of Charges. You must keep your own internal copy and update it whenever changes occur—these are not something you file and forget.

Can directors be held personally liable for not keeping proper records?

Yes, failure to maintain accounting records is a criminal offence under Section 285 of the Companies Act 2014. Directors can be held personally liable if it can be shown that failure to keep proper records contributed to the company's inability to pay its debts.

Do I need a written document retention policy?

A written document retention policy is not a legal requirement for most companies, but it is highly advisable. It demonstrates to the Data Protection Commission that your approach is considered and consistent rather than ad hoc, which can be important for GDPR compliance.