Close Company: Irish Tax Definition and Implications

Is your business a close company under Irish tax law? Check the five-participator test, the surcharges that can apply, and how to stay compliant.

Who should read this

Irish SME owners, directors of family businesses, accountants, and tax professionals handling private limited companies in Ireland should read this. It targets those unsure about company control structures and tax compliance.

Readers will gain clarity on close company definition, control tests, key tax surcharges and charges, exceptions, and practical steps for monitoring status and avoiding penalties through proper planning.

Key takeaways

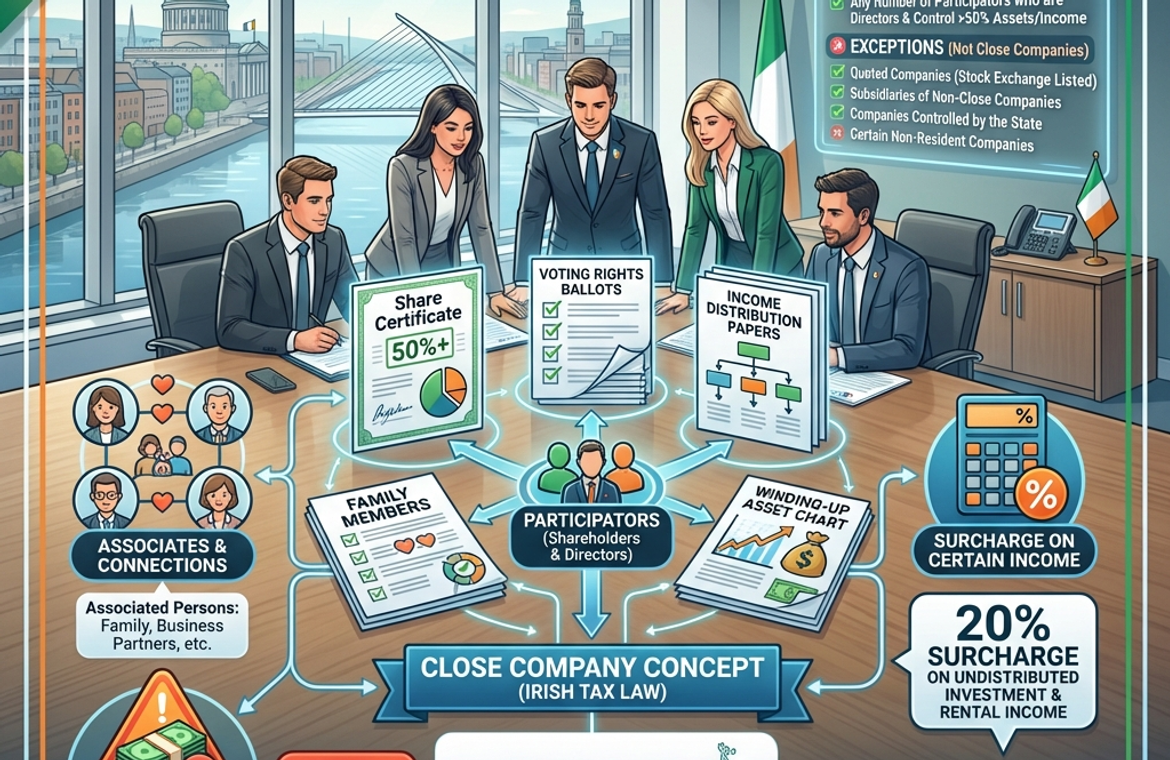

- A close company is under control of five or fewer participators or director-participators per Section 430 TCA 1997.

- Participators broadly include shareholders, loan creditors, and associates like family members.

- Tax implications include 20% surcharge on undistributed investment income and 25% on loans to participators.

- Professional service close companies face surcharges on undistributed profits if not distributed timely.

- Exceptions apply to quoted companies, non-residents without Irish trade, and subsidiaries of non-close companies.

What is a Close Company? Understanding the Irish Tax Definition

A close company is a specific type of private limited company identified under Irish tax law that receives particular tax treatment. Understanding whether your company qualifies as close is essential for compliance and tax planning purposes.

Legal Definition Under Irish Tax Law

Under Section 430 of the Taxes Consolidation Act 1997 (TCA 1997), a close company is defined as a company that is under the control of:

- Five or fewer participators, or

- Any number of participators who are also directors.

This definition applies to companies resident in Ireland for tax purposes and certain non-resident companies with an Irish trade connection.

The "Five or Fewer Participators" Test

The primary test examines who controls the company. A "participator" is broadly defined and includes shareholders, loan creditors, and anyone entitled to acquire shares or secure income distributions from the company.

Key points about the test:

The control threshold is met when five or fewer participators together own more than 50% of the following:

- Company's issued share capital,

- Voting rights,

- or rights to income or assets on a winding up.

Associates of participators are also counted, meaning family members and business partners can be grouped together when determining control. This makes the test broader than it might initially appear.

Determining If Your Company Is Close

To determine your company's status, you should examine the shareholding structure, identify all participators and their associates, calculate the combined control percentages, and consider whether any exceptions apply.

The practical reality is that the vast majority of Irish SMEs and family businesses qualify as close companies due to their concentrated ownership structures.

Tax Implications of Close Company Status

Close company status triggers several important tax considerations:

- Surcharge on undistributed investment income: Close companies that retain certain types of passive investment income may face a 20% surcharge on undistributed amounts, encouraging profit distribution to shareholders.

- Loans to participators: When a close company makes a loan to a participator or associate, the company must pay a tax charge of 25% of the loan amount to Revenue. This charge is refundable when the loan is repaid, but it represents a significant cash flow consideration.

- Professional Services Close company surcharge: Professional service close companies may face an additional surcharge on undistributed income if they don't distribute sufficient profits within 18 months of the accounting period end. For this surcharge, all undistributed professional profits are considered.

- Benefits to participators: Certain benefits provided to participators may be treated as distributions, affecting both the company and the individual's tax position.

Exceptions and Special Cases

- Not all private companies are close companies. Important exceptions include:

- Non-resident companies: Companies not resident in Ireland generally don't fall within the close company rules unless they carry on a trade in Ireland through a branch or agency.

- Quoted companies: Companies whose shares are listed on a recognised stock exchange as their ownership is typically too dispersed to meet the control tests.

- Companies controlled by non-close companies: If your company is controlled by another company that is not itself close (for example, a subsidiary of a publicly listed company), it may not be treated as close.

- Companies controlled by certain bodies: Companies under the control of specific entities like government bodies may be excluded from close company status.

Practical Considerations

For business owners and directors, close company status means maintaining awareness of several ongoing obligations. You should monitor loan accounts carefully to avoid unexpected tax charges, consider dividend policies in light of potential surcharges, maintain proper documentation of shareholding and control structures, and seek professional advice when making significant transactions with participators.

The close company rules reflect Revenue's concern that privately controlled companies might otherwise be used to shelter income from personal tax rates. While the rules add compliance obligations, they're manageable with proper planning and professional guidance.

If you're uncertain about your company's status or the implications of the close company rules for your specific circumstances, consulting with a tax advisor familiar with Irish corporate tax law is strongly recommended.

Irish Company Formation

Your Irish company, ready in days — not months.

Join 1,000+ founders who incorporated with Open Forest. We handle the paperwork, you focus on building.

No hidden fees/Fully compliant/Free consultation

Related articles

Mar 4, 2026 - 4 min read

What is venture debt? A guide for Irish startups

Venture debt lets VC-backed startups borrow without dilution—but comes with covenants and warrants. Here's how it works and when it makes sense.

Feb 10, 2026 - 4 min read

Convertible Loan Notes Explained: Complete Startup Guide

Learn how convertible loan notes work for Irish startups. Covers conversion mechanics, caps, discounts & when to use them. Expert guide.

Feb 9, 2026 - 6 min read

Pre-Money vs Post-Money Valuation: Complete Guide

Pre-money vs post-money valuation explained for founders. Learn how option pools affect dilution with real examples. Calculate your true ownership.

Frequently asked questions

Here's everything you need to know to get started, manage your account, and troubleshoot the most frequent issues.

A close company is defined under Section 430 of the Taxes Consolidation Act 1997 as a company under the control of five or fewer participators, or any number of participators who are also directors. This applies to Irish resident companies and certain non-residents with Irish trade.

The test checks if five or fewer participators control more than 50% of issued share capital, voting rights, or rights to income/assets on winding up. Participators include shareholders, loan creditors, and those entitled to shares or distributions. Associates like family are included.

Close companies face a 20% surcharge on undistributed investment income, 25% tax on loans to participators (refundable on repayment), surcharges for professional services companies on undistributed profits, and benefits to participators treated as distributions.

Exceptions include non-resident companies without Irish trade, quoted companies on stock exchanges, companies controlled by non-close companies or certain public bodies like government entities, due to dispersed ownership or other criteria.

Examine shareholding, identify participators and associates, calculate combined control over 50% in shares, votes, or assets. Most Irish SMEs and family businesses qualify due to concentrated ownership.

Questions are welcome.

We’ll point you in the right direction.

Share a few details below and our team will follow up with guidance for your Ireland or UK company.