This article is for Irish startup founders who are negotiating investment terms and need to understand what anti-dilution protection means for their ownership.

If you're facing a term sheet with anti-dilution clauses and wondering how they'll affect you in a down round, this guide covers the different types of protection (full ratchet vs. weighted average), when they trigger, and how to negotiate terms that don't destroy your equity position.

Key Takeaways

• Negotiate for broad-based weighted average anti-dilution protection as market standard, avoiding full ratchet except in emergency funding situations. • Anti-dilution protection activates during down rounds, giving investors additional shares without new capital and increasing founder dilution significantly. • Include carve-outs for employee option pools, strategic acquisitions, and conversions to prevent routine transactions from triggering anti-dilution provisions. • Negotiate sunset provisions that terminate anti-dilution protection after specific milestones or time periods to limit long-term impact. • Create employee option pools before investment rounds to spread dilution across all shareholders rather than concentrating it on founders.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

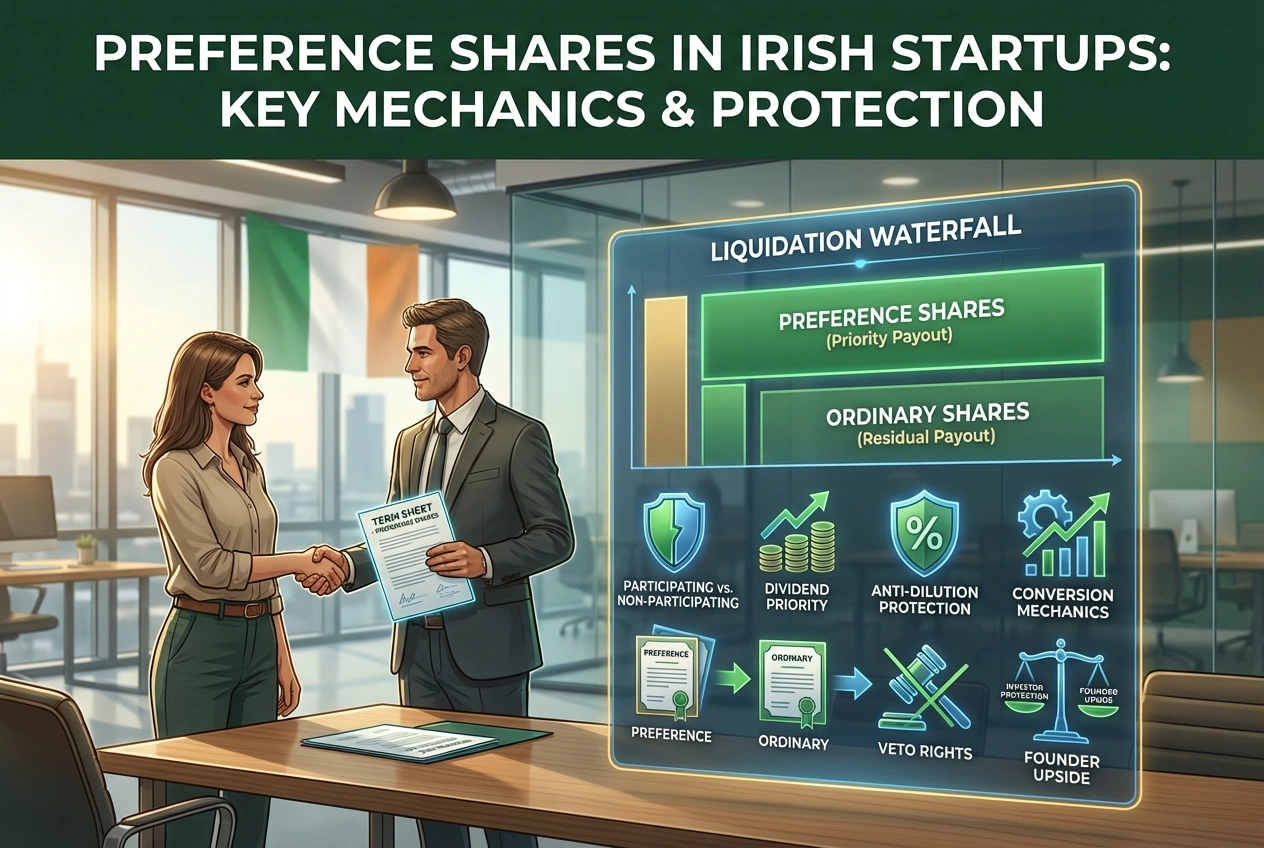

What exactly is anti-dilution protection and when does it kick in?

Anti-dilution protection is a contractual right that adjusts how many shares investors receive if you raise funding at a lower price than they originally paid. It activates during "down rounds" when new shares are sold at a lower price per share than previous investors paid, preventing their ownership from being economically diluted.

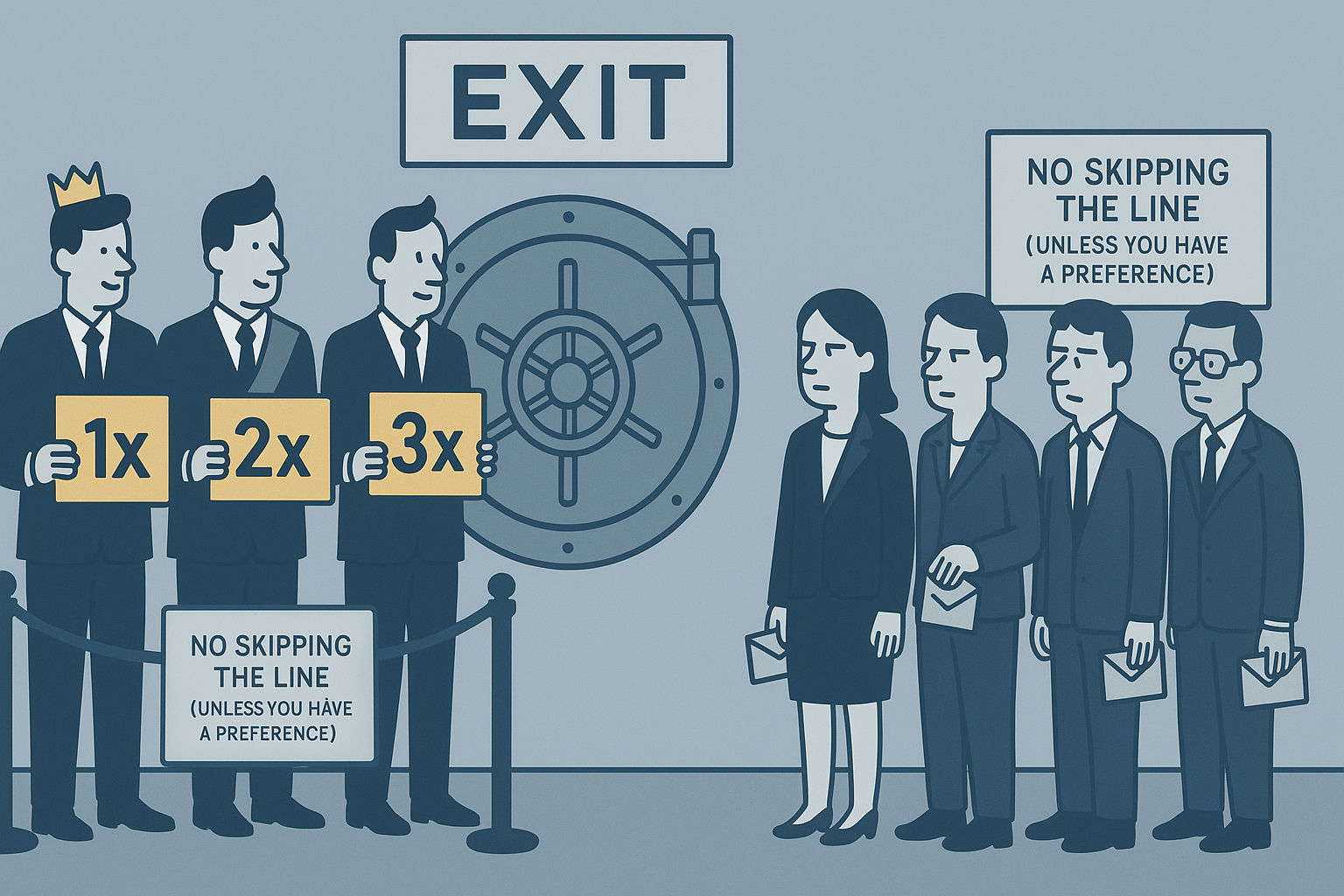

Should I accept full ratchet anti-dilution protection to close a deal quickly?

Full ratchet should only be considered in bridge rounds or emergency funding situations, as it's the most aggressive form that can crush founder ownership. If an investor paid €10 per share and you later raise at €2, their entire investment gets repriced at €2, giving them five times as many shares—most sophisticated investors recognize this destroys founder motivation.

What's the difference between broad-based and narrow-based weighted average protection?

Broad-based weighted average includes all outstanding shares, options, and convertible securities in the calculation, making it the most common and founder-friendly option in Irish investment agreements. Narrow-based uses the same formula but excludes options and convertible securities, resulting in slightly stronger protection for investors and more dilution for founders.

Will issuing employee stock options trigger my investors' anti-dilution protection?

No, employee option pools are typically excluded from anti-dilution calculations in most agreements. Issuing shares to employees under approved option schemes won't trigger protection, which is essential for recruiting and incentivizing key team members without penalizing yourself.

How can I negotiate better anti-dilution terms without scaring off investors?

Push for broad-based weighted average as your starting position since it represents market standard for Irish startup investments. You can also negotiate a sunset provision that terminates protection after hitting specific milestones, include a 10-20% minimum threshold before protection triggers, or limit protection to only the next funding round rather than all future issuances.

What happens to my ownership percentage when anti-dilution protection is triggered?

When protection triggers, you must issue additional shares to protected investors without receiving new capital, meaning founders and employees holding ordinary shares suffer increased dilution. The anti-dilution provisions essentially transfer economic dilution from investors to common shareholders, primarily founders.

Do strategic transactions like acquiring another company trigger anti-dilution protection?

Most agreements include carve-outs where issuing shares to acquire another company or secure partnerships may be excluded from triggering protection. You should negotiate broad carve-outs for strategic transactions during the initial investment to avoid triggering protection when making moves that benefit the company.

Can I get rid of anti-dilution protection once my company is performing well?

Yes, you can negotiate a sunset provision that terminates protection after a specified period or milestone, as anti-dilution becomes less relevant once you've demonstrated product-market fit. You can also include performance milestones where hitting revenue or user targets eliminates the provisions, or reserve rights to buy out the protection at a predetermined price if you later have resources.

.webp)