This article is for startup founders in Ireland who are raising their first funding round and need to understand how investor valuations actually work.

If you're confused about pre-money vs post-money valuations, how option pools affect your ownership, or why two similar-looking term sheets can leave you with very different equity stakes, this guide breaks down the math, shows real calculation examples, and explains exactly what questions to ask investors before signing anything.

Key Takeaways

• Pre-money valuations place option pools before investor dilution, reducing founder ownership more than post-money valuations with identical headlines. • Always calculate your final ownership percentage after investment and option pool creation, not just the headline valuation number. • Post-money valuations have become standard in Irish early-stage deals, making investor ownership percentages immediately transparent without additional calculations. • A 15% option pool under pre-money valuation can cost founders 3-5% more ownership than the same pool under post-money terms. • Request a fully-diluted cap table showing exact ownership percentages before signing any term sheet to avoid costly surprises.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

What's the difference between pre-money and post-money valuation?

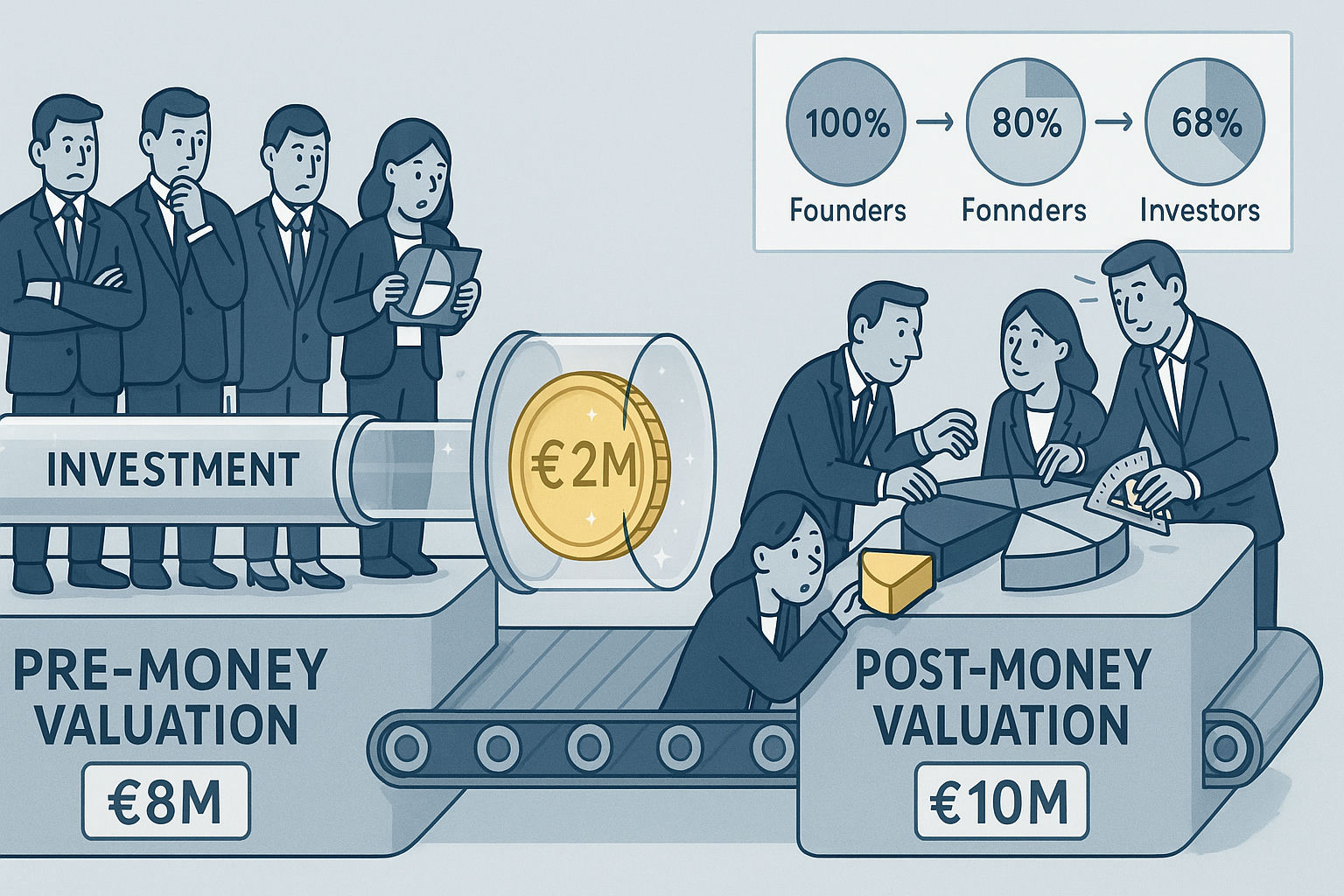

Pre-money valuation is what your company is worth before new investment arrives, while post-money valuation is the total value after the investment lands. If an investor offers €2 million at €8 million pre-money, your company is worth €8 million before their money, and €10 million post-money (€8M + €2M). The key difference is that post-money valuation makes the investor's ownership percentage immediately obvious without additional calculation.

How does the option pool affect my ownership differently under pre-money vs post-money valuation?

Under pre-money valuation, the option pool dilutes only founders before the investor takes their percentage, while under post-money valuation, the pool dilutes both founders and investors proportionally. For example, with a 15% option pool requirement, pre-money valuation means you lose ownership to both the pool and the investor separately, while post-money means the investor shares the dilution burden with you. This difference can cost founders several percentage points of ownership.

Which valuation method is more common in Irish startup deals?

Post-money valuations have become increasingly standard in Irish early-stage term sheets, aligning with broader European and US market trends toward simpler, founder-friendly structures. However, pre-money valuations still appear regularly in later-stage deals and institutional investor term sheets. Always verify which method any term sheet uses before comparing offers, as you should never assume.

Can two offers with the same headline valuation give me different ownership outcomes?

Yes, absolutely. Two €10 million valuations can produce vastly different ownership outcomes depending on whether they're pre-money or post-money and how the option pool is treated. For example, €2 million at €8 million pre-money with a 10% pre-money option pool leaves founders with 72% ownership, while €2 million at €9 million post-money with a 10% post-money pool leaves founders with only 70% ownership, despite the higher headline valuation.

What's my actual ownership percentage after a typical seed round?

Using the article's example, if you start with 100% ownership and raise €2 million at €8 million pre-money with a 15% option pool, you'll end up with 68% ownership. The investor takes 20%, the option pool accounts for 12%, and you've been diluted by 32% total. Your final ownership percentage matters far more than the headline valuation number when evaluating term sheets.

What questions should I ask investors when reviewing a term sheet?

You should explicitly ask: Is this pre-money or post-money valuation? Is the option pool included in the valuation? What's my ownership percentage after this round closes? Always get confirmation in writing and request a fully-diluted cap table showing exactly how all shares and options calculate. Understanding whether terms are market-standard also helps in negotiations.

How do I properly compare competing investment offers?

Convert all offers to the same valuation basis and focus on your final ownership percentage rather than headline valuation numbers. Calculate your ownership after accounting for both the investor's stake and the option pool under each offer's specific terms. Create a spreadsheet showing the complete cap table to see the real economic impact of each deal structure.

What happens to my ownership in future funding rounds?

Future rounds will dilute you further beyond the current round's dilution. A 70% stake after your seed round typically becomes 50% after Series A and 35% after Series B. You should model your cap table showing ownership after each anticipated funding round to ensure you'll maintain meaningful ownership through exit, as many founders discover too late they've diluted below viable ownership levels.

.webp)