This article is for Irish startup founders preparing to raise investment who need to get their share capital structure investor-ready.

If you're wondering what share structure investors expect, how to clean up your cap table, or when to implement preference shares and vesting arrangements, this guide covers the pre-investment restructuring steps that prevent due diligence delays and deal-breakers.

Key Takeaways

• Start with ordinary shares for founders and a single share class to keep your structure simple and minimise costs.

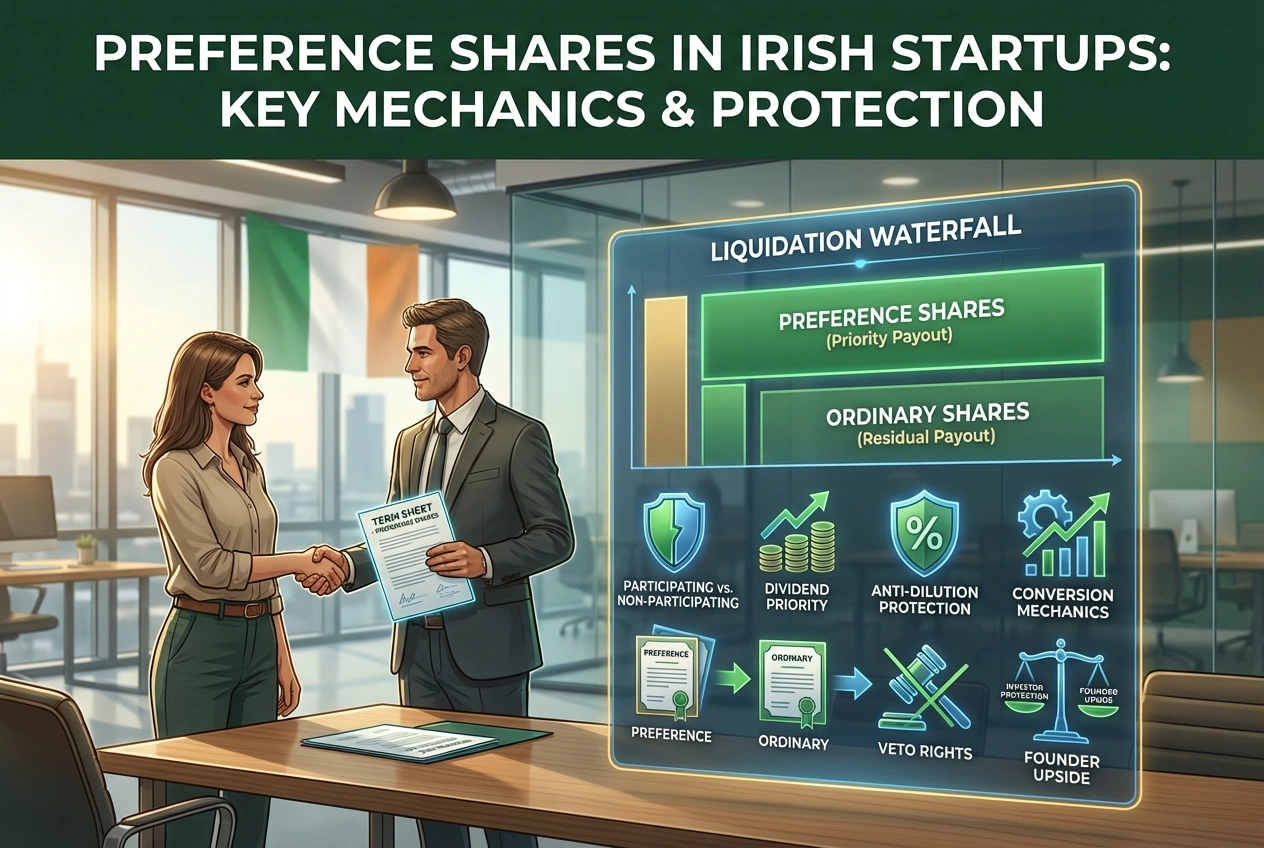

• Investors require preference shares with liquidation preference, conversion rights, and anti-dilution protection to protect their investment.

• Create an employee option pool of 10-15% before investment, as this dilutes founders rather than investors and is market standard.

• Implement founder share vesting over 3-4 years with a one-year cliff before approaching investors to demonstrate commercial awareness.

• Clean up obvious problems like missing share certificates before fundraising, but wait for a signed term sheet before implementing full investor structure.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

Should I create preference shares when I first incorporate my company?

You can start with just one class of ordinary shares to keep things simple and minimize costs initially. However, creating preference shares at incorporation can save time later since investors will require them anyway, and you'll need to amend your constitution through a special resolution (75% shareholder vote) if you add them later.

What's the ideal share capital structure before approaching investors?

Your pre-investment structure should include ordinary shares for founders with proper documentation, a single share class initially, and adequate authorized share capital to avoid constitutional amendments at each funding round. All founders should have signed founders agreements documenting their investment and any vesting arrangements to prevent disputes.

Why do investors insist on preference shares instead of ordinary shares?

Preference shares protect investors from downside risk while preserving upside potential through specific rights: dividend preference, liquidation preference (getting their money back first if the company is sold), conversion rights to ordinary shares on exit, and anti-dilution protection. This structure gives them better returns in success while limiting losses if the company fails.

Do I need to create an employee share option pool before raising investment?

Yes, investors typically require you to create an option pool of 10-15% of fully diluted share capital before investment to ensure employee incentives don't dilute their stake. The option pool dilutes founders rather than investors, which is market standard, and pushing back on this rarely succeeds and signals inexperience with fundraising norms.

What are tag-along and drag-along rights, and why do investors require them?

Tag-along rights let investors sell their shares alongside founders if founders receive a purchase offer, preventing founders from exiting while investors remain stuck in the company. Drag-along provisions let majority shareholders (typically 75% threshold) force minority shareholders to join in approved sales, ensuring small shareholdings don't block valuable exit opportunities.

Should I implement founder vesting before or after talking to investors?

Implement founder vesting (typically 3-4 years with a one-year cliff) before approaching investors, as this will definitely be required and demonstrates commercial awareness. However, wait until you have a signed term sheet before creating preference shares and complex constitutional provisions, since the term sheet will specify exactly what structure investors need.

What documentation should I have ready for investor due diligence?

You need your current constitution showing all share classes, share certificates for all issued shares, register of members, register of directors, all subscription agreements, and board minutes approving share issues. Your cap table should clearly show all shareholders and ownership percentages on both issued and fully diluted basis, including all options with exercise prices and vesting schedules.

What happens if I set my authorized share capital too low?

Setting authorized capital too low means you'll need to amend your constitution before each funding round, which creates delays and costs. Setting it higher at incorporation costs nothing but provides flexibility when you need it, so it's better to give yourself room for growth from the start.

.webp)