This article is for startup founders in Ireland who are negotiating their first investment term sheet and need to understand what they're actually agreeing to.

If you're wondering which terms are binding immediately, how vesting schedules work, what liquidation preferences mean, or which investor demands you should push back on, this guide breaks down every major provision from option pools to board composition to protective provisions.

Key Takeaways

• Exclusivity and confidentiality clauses are immediately binding upon signing, while economic terms only bind when definitive agreements are signed weeks later. • Negotiate partial vesting credit if you've worked on the company before investment, reducing the standard four-year vesting period proportionally. • Insist on 1x non-participating liquidation preferences and reject participating or multiple preferences that let investors get paid twice. • Push back on pre-money option pools exceeding 12-18 months of realistic hiring needs, as each percentage point directly dilutes your ownership. • Ensure the independent board director requires mutual approval, as this person breaks deadlocks between founders and investors on critical decisions.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

Which parts of a term sheet are actually binding when I sign it?

Only the exclusivity and confidentiality provisions are binding immediately upon signing. The exclusivity period (typically 30-90 days) prevents you from negotiating with other investors, while confidentiality provisions restrict what you can disclose about the terms. All economic and governance terms only become binding weeks later when you sign the definitive investment agreements.

What happens to my shares if I leave the company before the vesting period ends?

You'll forfeit any unvested shares back to the company. Standard vesting includes a one-year cliff, meaning you must stay for 12 months to earn any shares (25% after year one), then the remaining 75% vests monthly over the next three years. If you've been working on the company before raising investment, negotiate partial credit for this time served.

Should I accept single trigger or double trigger acceleration in my term sheet?

Double trigger acceleration is now the market standard and actually works better for you. While single trigger (vesting all shares immediately upon acquisition) sounds founder-friendly, it can kill acquisition deals because acquirers don't want founders receiving all equity upfront. Double trigger requires both an acquisition and termination without cause, which protects you while keeping deals viable.

How does the option pool affect my ownership percentage?

If the term sheet specifies the option pool on a "pre-money basis," that pool comes entirely from your founder shares before calculating the investor's percentage, meaning you bear the full dilution cost. A 15% pre-money option pool costs you real ownership that you might never actually use for employees. Push back on pools exceeding realistic hiring needs over the next 12-18 months.

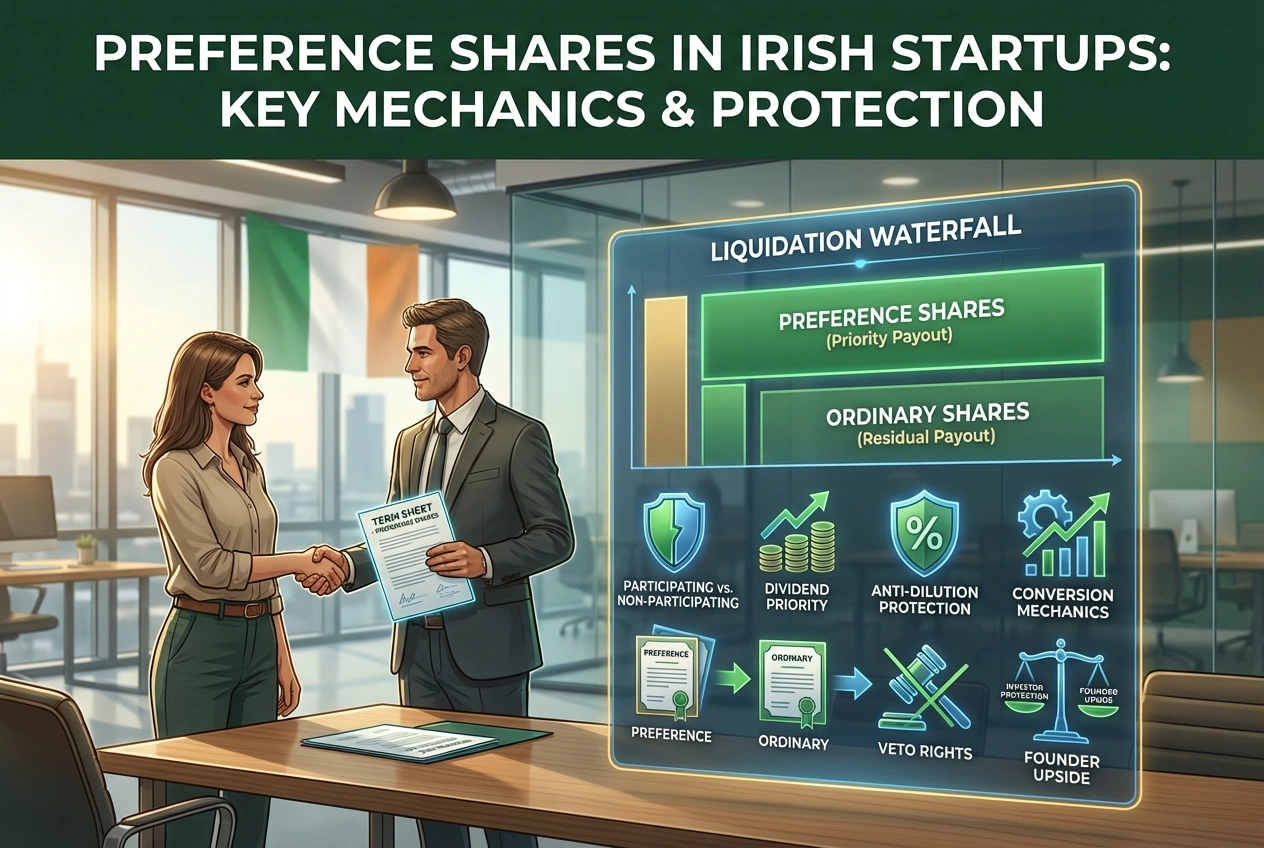

What's the difference between participating and non-participating liquidation preferences?

A 1x non-participating preference (the market standard) means investors get their investment back first, then remaining proceeds distribute to everyone based on ownership percentages. Participating preferences let investors receive their preference amount plus their pro-rata share of remaining proceeds—effectively getting paid twice—and should be strongly resisted except in rescue financing situations.

How much control do board seats actually give investors?

Board seats provide more practical control than voting percentages because the board makes operational decisions while shareholder votes typically only matter for major corporate actions. The independent director selection process matters enormously because that person breaks deadlocks between founders and investors, so negotiate clear criteria and mutual approval rights rather than allowing either side unilateral appointment power.

What protective provisions should I expect investors to request?

Standard protective provisions cover genuinely major decisions like selling the company, raising additional funding, issuing new share classes, or changing the business purpose. Push back on excessive provisions requiring investor approval of budgets, hiring decisions, individual expenses, or opening new office locations—these operational matters belong under board oversight, not specific investor approval.

Can early investors' pro-rata rights complicate my future fundraising?

Yes, pro-rata rights allow early investors to maintain their ownership percentage in future rounds, but if all your seed investors exercise these rights, less room remains for new lead investors in your Series A. This can potentially kill deals or require a larger round than optimal, so consider limiting pro-rata rights to major investors only.

.webp)

.webp)