International executives and companies planning expansion into Ireland, especially in professional services, manufacturing, holding, or service sectors seeking to understand legal structures.

Readers will gain clarity on liability, tax, setup, compliance, IP, and HR differences to choose optimal branch or subsidiary for risk management and efficiency.

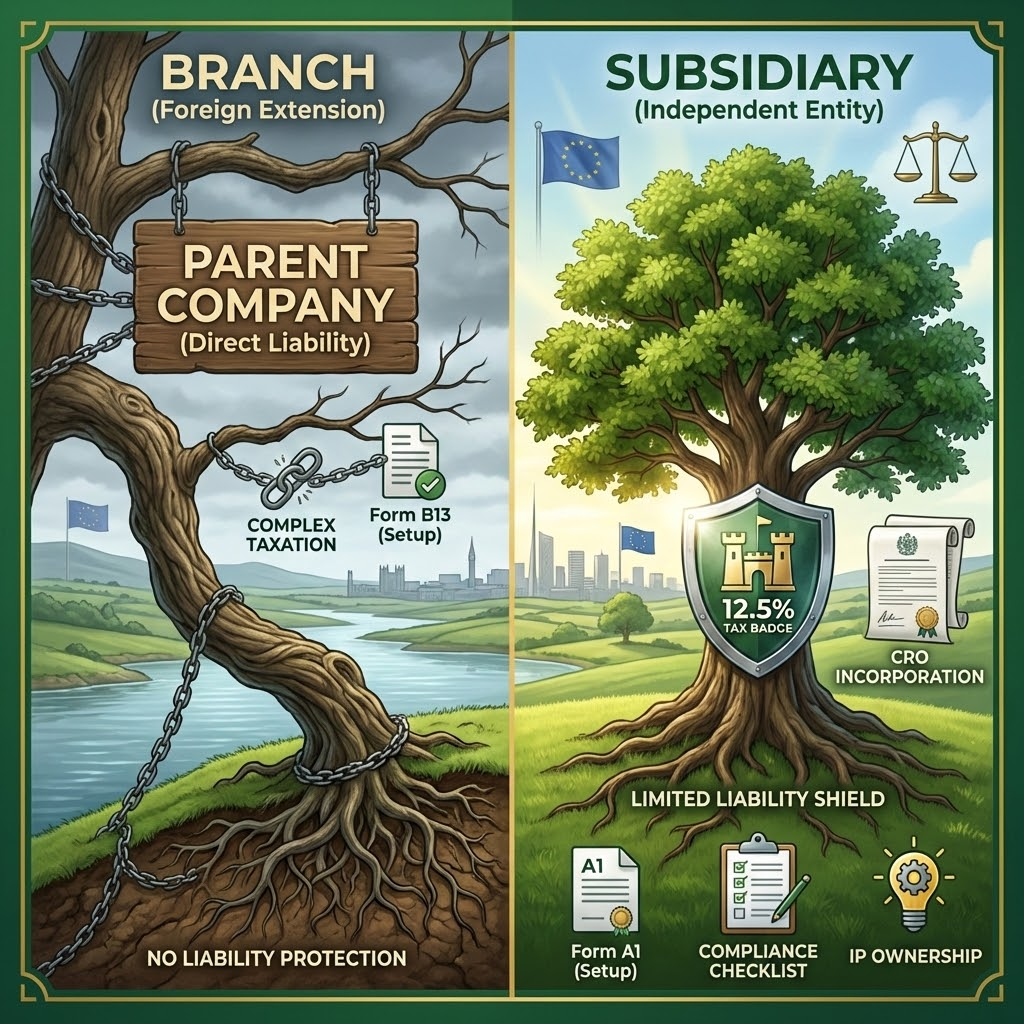

What's the Fundamental Difference Between a Branch and Subsidiary? A subsidiary is a separate Irish company that you own and control.

A branch is simply an extension of your existing foreign company operating in Ireland.

This distinction affects everything from liability protection to tax treatment. Your subsidiary exists as an independent legal entity under Irish law, while your branch remains part of your parent company with no separate legal personality.

The choice between these structures determines your risk exposure, tax obligations, and operational flexibility.

How Does Limited Liability Differ Between the Structures? Subsidiaries provide complete separation between your parent company and Irish operations.

Section 38 of the Companies Act 2014 establishes that private limited companies have full legal capacity separate from their shareholders . This means your parent company's liability is limited to its investment in the subsidiary's share capital.

Branches offer no liability protection because they're not separate legal entities. Any debts, obligations, or legal claims against your Irish branch become direct liabilities of your parent company. Your parent company's global assets could be exposed to claims arising from Irish branch operations.

This difference matters most when operations involve significant risk. If your Irish activities could generate product liability claims, employment disputes, or contractual liabilities, subsidiary structure protects your parent company from these exposures.

What Are the Tax Implications of Each Structure? Irish subsidiaries pay Ireland's 12.5% corporate tax rate on trading income.

This competitive rate applies to profits generated by the Irish subsidiary, making Ireland attractive for European operations. The subsidiary files Irish tax returns as a standalone Irish resident company.

Branch taxation proves more complex because branches aren't separate entities. Your branch's Irish activities may create tax obligations in Ireland, but the branch doesn't file as a separate taxpayer. Instead, the parent company reports branch income in its home jurisdiction while potentially owing Irish tax on branch profits.

Transfer pricing rules affect subsidiaries differently than branches. When your subsidiary transacts with your parent company, arm's length pricing applies.

Double taxation treaties between Ireland and your home country determine final tax treatment. These treaties prevent paying full tax in both jurisdictions, but the mechanics differ significantly for branches versus subsidiaries.

How Do Setup Requirements Compare? Establishing an Irish subsidiary requires full company incorporation through the Companies Registration Office.

You must appoint at least one EEA-resident director or purchase a Section 137 bond, designate a company secretary, establish an Irish registered office address, and file Form A1 with constitutional documents. The process typically takes 5-10 working days once all requirements are met.

Branch registration involves filing specific forms with the CRO within one month of commencing Irish activities. Key requirements include:

Filing Form B13 containing parent company details

Providing certified copies of parent company constitutional documents

Appointing at least one authorised representative in Ireland

Establishing an Irish business address

Registering with Revenue for applicable taxes

EU companies benefit from simplified procedures under European Communities regulations. Non-EU companies face additional documentation requirements including notarised and translated documents proving parent company legal status.

What Ongoing Compliance Obligations Apply? Irish subsidiaries face standard company compliance requirements under the Companies Act 2014.

These include filing annual returns within six months of your Annual Return Date, preparing and filing Irish financial statements, maintaining statutory registers at the registered office, and holding general meetings as required by your constitution.

Branches must file annual returns containing parent company accounts including preparing and filing documents about their entire global business, not just Irish operations.

Directors of Irish subsidiaries have statutory duties under Sections 228-234. These include duties to act in good faith in the company's interests, avoid conflicts of interest, and not use company property for personal benefit.

Both structures must register for applicable Irish taxes including corporation tax, VAT, and employer taxes if hiring staff. However, tax compliance complexity differs significantly based on the structure chosen.

How Do Regulatory Requirements Differ by Industry? Certain regulated activities require specific licenses or authorizations regardless of structure.

Financial services, insurance, and payment services need Central Bank authorization. These regulations typically require Irish legal entity establishment, effectively mandating subsidiary structure for regulated activities.

Data protection obligations under GDPR apply equally to both structures. However, subsidiaries establish clearer data controller/processor relationships, simplifying compliance when transferring data between Irish operations and parent companies.

Employment law applies identically whether you operate as branch or subsidiary. Irish employment legislation protects employees working in Ireland regardless of employer structure.

Industry-specific regulations may favour one structure over another. Professional services often prefer subsidiaries for liability protection, while consulting firms might use branches for simpler operations with lower risk profiles.

Which Structure Suits Different Business Types? Most international companies expanding into Ireland choose subsidiary structure.

The liability protection, clear tax treatment, and operational flexibility outweigh higher setup costs. Subsidiaries suit companies with:

Significant Irish operations requiring multiple employees

Activities carrying liability risks like manufacturing or professional services

Plans for substantial Irish market investment

Desire for permanent Irish establishment

Need to raise capital or issue shares to Irish employees

Branches make sense in limited circumstances. Consider branch structure when:

Testing Irish market before committing to full subsidiary

Providing limited services to existing clients from your home jurisdiction

Operating short-term projects with defined end dates

Parent company maintains tight operational control requirements

Regulatory requirements prevent subsidiary establishment

Holding companies typically use subsidiary structures. Subsidiary structure provides clear ownership chains and simplified corporate governance.

Service companies often prefer subsidiaries despite lower perceived risk. The professional credibility of Irish company registration, combined with banking and contracting advantages, makes subsidiaries worthwhile even for consulting or professional services with limited physical assets.

What About Intellectual Property Considerations? Subsidiaries can own Irish intellectual property separately from parent companies.

This creates strategic opportunities for IP structuring across jurisdictions.

Can Irish Subsidiaries Own IP Separately? Yes, Irish subsidiaries function as independent legal entities that can own intellectual property. Your subsidiary can hold European IP rights while the parent company retains rights in other territories.

This separation allows strategic positioning of valuable assets within your corporate group. Transfer pricing rules govern how you license IP between parent and subsidiary companies.

Revenue scrutinises these arrangements to ensure arm's length pricing.

What IP Rights Do Branches Have? Branches cannot own IP separately from the parent company.

Any intellectual property developed or used by your Irish branch belongs to the parent company automatically.

This happens because branches lack separate legal personality under Irish law.

The simplified ownership structure reduces administrative complexity.

It eliminates the structuring flexibility that subsidiaries provide.

How Do Employment and HR Considerations Differ? Irish employment law applies equally whether you operate as branch or subsidiary.

Both structures must comply with minimum wage requirements, working time regulations, health and safety standards, and employee rights legislation. The employer's legal structure doesn't affect employee protections.

However, employment contract clarity differs. Subsidiary employees work for an Irish company with straightforward employment relationships. Branch employees technically work for a foreign company operating in Ireland, potentially complicating contracts and benefits administration.

Pension auto-enrolment regulations coming into effect will apply to both structures. However, subsidiaries can establish Irish pension schemes more easily than branches, which might need to coordinate with parent company pension arrangements.