Employees under PAYE, self-employed traders, landlords with rental income, investors receiving dividends or deposit interest, and property sellers facing CGT—all residents or taxpayers in Ireland.

This guide provides detailed tax treatments, 2026 rates, credits like personal/employee €2,000, deductions, reliefs, and deadlines to ensure accurate filing, avoid penalties, and optimize tax positions.

Key Takeaways

Progressive income tax: 20% up to €44,000 (single)/€53,000 (married one earner), 40% above for 2026.

USC rates tiered 0.5% to 8%; exempt <€13,000; 11% on non-PAYE >€100,000; reduced for seniors/medical card.

Employment PRSI Class A 4.2% employee/employer up to 11.25%; self-employed Class S 4.2%.

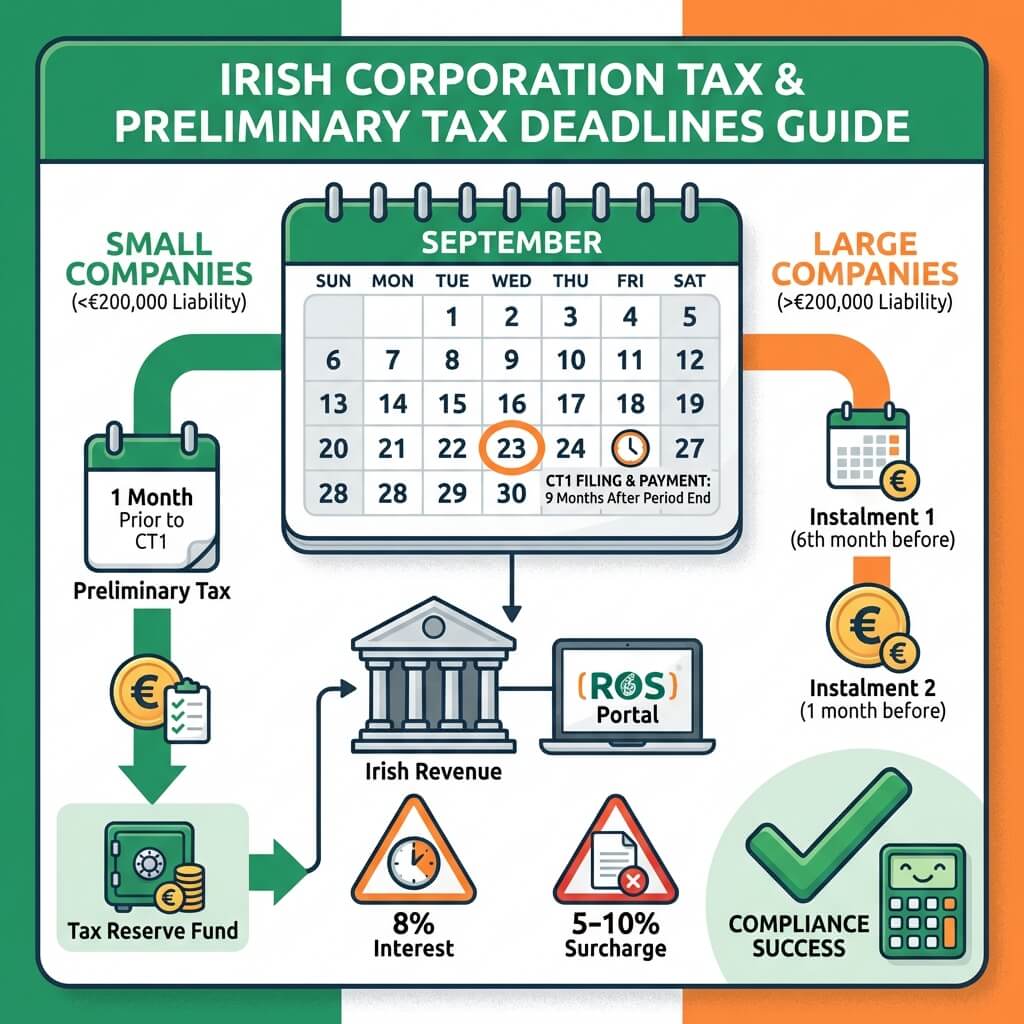

Self-employed deduct business expenses, claim earned income credit; pay preliminary tax Oct 31.

Paul Burke is a qualified ACA and CTA tax accountant in Ireland.He trained at Forvis Mazars in Galway, gaining experience in various tax heads including Income Tax, Corporation Tax, VAT, Payroll and Tax Advisory.He is now a Tax Consultant in a local tax firm.

What are the income tax rates in Ireland for 2026?

The standard rate is 20% on income up to €44,000 for single individuals and €53,000 for married couples or civil partners with one income. Income above these thresholds is taxed at 40%. Key credits include €2,000 personal tax credit and €2,000 employee tax credit for singles, €4,000 for married.

How is USC calculated on income in Ireland?

USC applies to gross income: 0.5% on first €12,012, 2% from €12,012 to €28,700, 3% to €70,044, 8% above €70,044. Exempt if total income ≤€13,000. Non-PAYE over €100,000 has 3% surcharge to 11%. Reduced rates for 70+ or medical card holders with ≤€60,000 income.

What are preliminary tax obligations for self-employed in Ireland?

Self-employed must estimate and pay preliminary tax by October 31, at minimum the lower of 90% current year liability, 100% previous year, or 105% pre-previous if direct debit. Final return and balance due next October 31. Insufficient payment incurs 8% interest.

What is Rent-a-Room Relief in Ireland?

Rent-a-Room Relief exempts income up to €14,000 per year from renting a room in one's principal private residence from income tax, USC, and PRSI. If rent exceeds €14,000, the entire amount becomes taxable. Landlords must register with Residential Tenancies Board.

How does Capital Gains Tax work in Ireland?

CGT is 33% on gains from asset disposals (proceeds minus cost and expenses). Annual €1,270 exemption per person. Losses offset same-year gains or carry forward. Principal Private Residence Relief for main home. Due Dec 15 (Jan-Nov disposals) or Jan 31 (Dec).