Irish business owners, accountants, finance directors, and tax professionals handling corporation tax returns for companies.

Readers will gain insights into profit adjustments, deductible vs. non-deductible expenses, capital allowances, R&D credits, and compliance tips to minimize tax liability and maximize reliefs.

Key Takeaways

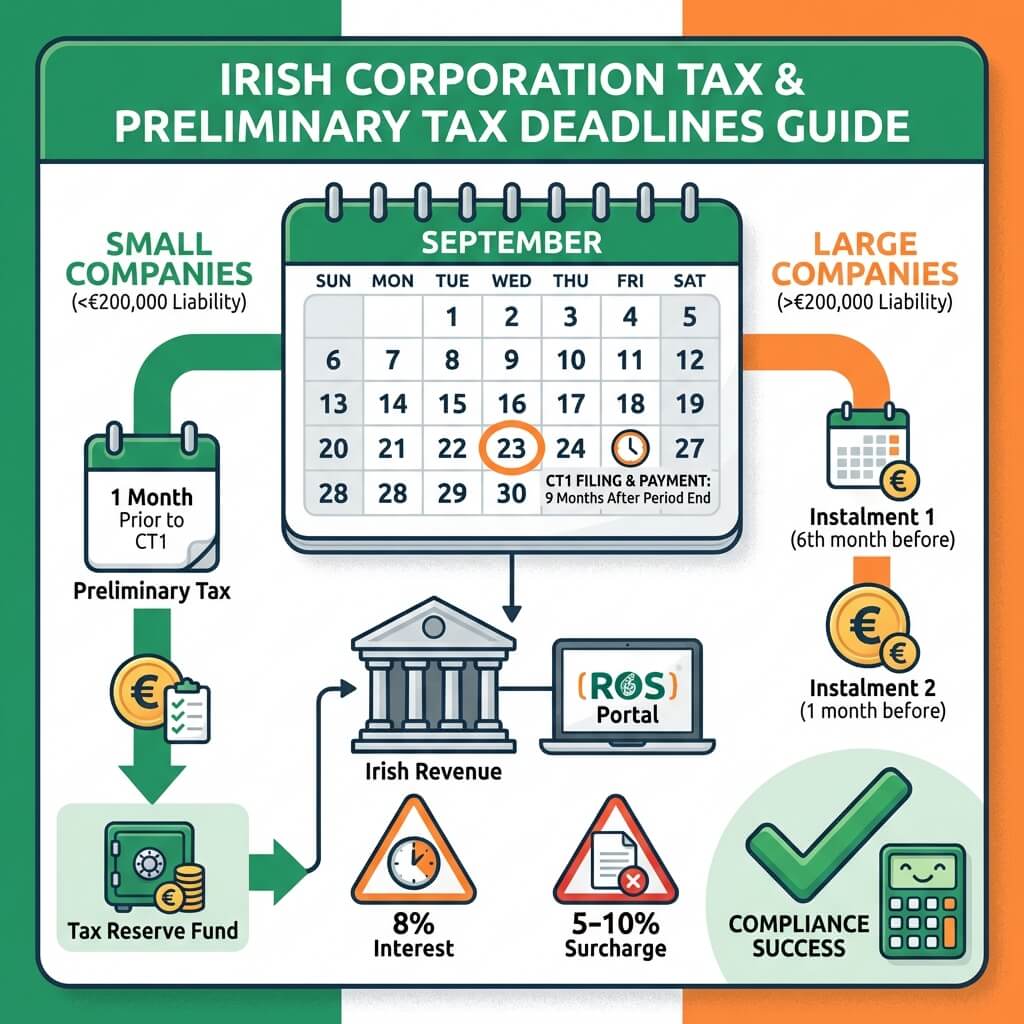

Start with accounting profit, add back non-deductibles like depreciation, entertainment, fines, then deduct capital allowances and reliefs to reach tax-adjusted profit.

Capital allowances replace depreciation: 12.5% for plant/machinery, 100% for energy-efficient, 4% industrial buildings.

R&D tax credit at 35% provides significant relief on qualifying expenditure, claimable as cash refunds.

Trading losses carry forward indefinitely, back one year, or via group relief.

Expenses must be 'wholly and exclusively' for trade; client entertainment out, staff welfare in.

Paul Burke is a qualified ACA and CTA tax accountant in Ireland.He trained at Forvis Mazars in Galway, gaining experience in various tax heads including Income Tax, Corporation Tax, VAT, Payroll and Tax Advisory.He is now a Tax Consultant in a local tax firm.

What is added back for depreciation in Irish corporation tax?

Depreciation is added back to accounting profit as it is not deductible. Instead, capital allowances provide tax depreciation at 12.5% straight-line for plant and machinery over eight years, e.g., €3,125 annually for a €25,000 asset. Motor vehicles limited to €24,000, with energy-efficient options at 100% first-year relief.

Why are entertainment expenses non-deductible?

Client entertainment like dinners, gifts, and hospitality is non-deductible and must be added back. However, staff welfare such as Christmas parties and team-building is allowable as employee benefits under the 'wholly and exclusively' trade purpose rule.

How do capital allowances work for intellectual property?

Capital allowances for patents, trademarks, know-how follow accounting amortization or 15-year claim, ring-fenced to IP income with 80% annual limit. Energy-efficient equipment gets 100% first-year relief; industrial buildings 4% annually.

What is the R&D tax credit in Ireland?

The R&D credit is 35% (Budget 2026) on qualifying spend like staff, materials, buildings (35% R&D use), plus 12.5% deduction for 47.5% benefit. Outsourced up to €100k or 15%. Claim as cash refund over three periods, threshold €87,500 first year.

Can trading losses be carried back?

Trading losses carry forward indefinitely against same trade profits or back one year against all profits. Group relief allows surrender between 75% owned Irish group companies.