This guide is essential for directors, finance managers, and accountants of Irish companies handling Corporation Tax obligations, especially small and large firms navigating preliminary tax payments.

Readers will learn precise deadlines, calculation methods, penalties for non-compliance, and proven strategies like tax reserves and reliefs to optimize cash flow and ensure Revenue compliance.

Key Takeaways

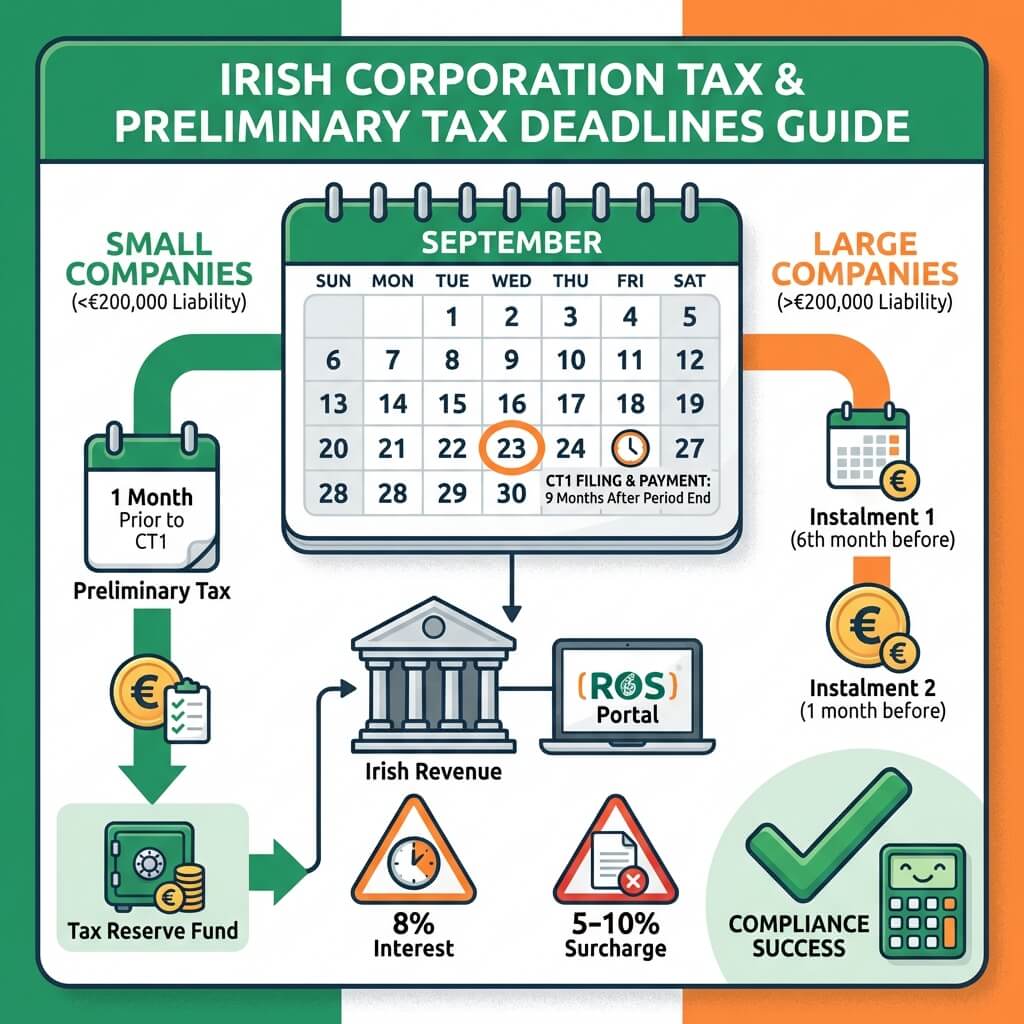

Corporation Tax returns must be filed by the 23rd day of the 9th month after accounting period end.

Small companies pay Preliminary Tax one month before period end; large companies in two instalments.

Preliminary Tax: 90% current or 100% prior year to avoid interest.

Late filing: 5-10% surcharges; late payment: 8% interest per annum.

Manage cash flow with forecasting, reserves, professional advice, and relief claims.

Paul Burke is a qualified ACA and CTA tax accountant in Ireland.He trained at Forvis Mazars in Galway, gaining experience in various tax heads including Income Tax, Corporation Tax, VAT, Payroll and Tax Advisory.He is now a Tax Consultant in a local tax firm.

What is the filing deadline for Corporation Tax returns?

Companies must file their Corporation Tax Return (Form CT1) on or before the 23rd day of the 9th month after the accounting period end via ROS. For example, for period ending 31 December 2025, file by 23 September 2026. Outstanding liability is also due then.

What is Preliminary Tax?

Preliminary Tax is an advance payment based on the company's estimate of its Corporation Tax liability for the current year. It is subtracted from the final tax due; overpayments are refunded by Revenue.

What are Preliminary Tax deadlines for small companies?

Small companies (preceding CT liability ≤ €200,000) pay Preliminary Tax by the 23rd of the month prior to accounting period end. Amount: 100% prior year or 90% current year liability.

What penalties apply for late Corporation Tax payment?

Interest at 8% per annum (0.0219% daily) on late payments from due date. Late filing surcharges: 5% if within 2 months, 10% if over 2 months, with caps at €12,695 and €63,485.

How can companies avoid tax compliance issues?

Use accurate forecasting, tax reserve funds, prior year basis for small firms, claim reliefs like R&D credits, engage advisors, and consider phased payments if needed. Maintain records and meet deadlines.