This article is for startup founders, investors, and shareholders who need to understand how drag-along and tag-along rights work in shareholder agreements.

If you're negotiating investment terms, facing a potential company sale, or wondering how these provisions protect (or expose) you during an exit, this guide covers how drag-along rights force minority shareholders to sell, how tag-along rights protect minorities from being left behind, and what happens when these rights are triggered in real acquisition scenarios.

Key Takeaways

• Drag-along rights allow majority shareholders (typically holding 51-75%) to force minorities to sell their shares during company acquisitions. • Tag-along rights protect minority shareholders by letting them sell on identical terms when majority shareholders exit the company. • Buyers typically pay 20-30% control premiums for 100% ownership, making drag-along rights valuable for maximizing sale proceeds. • Founders should negotiate tag-along protection before losing majority control through multiple funding rounds to preserve exit options. • Well-drafted provisions must specify ownership thresholds, notice periods, permitted consideration types, and warranty limitations to prevent disputes.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

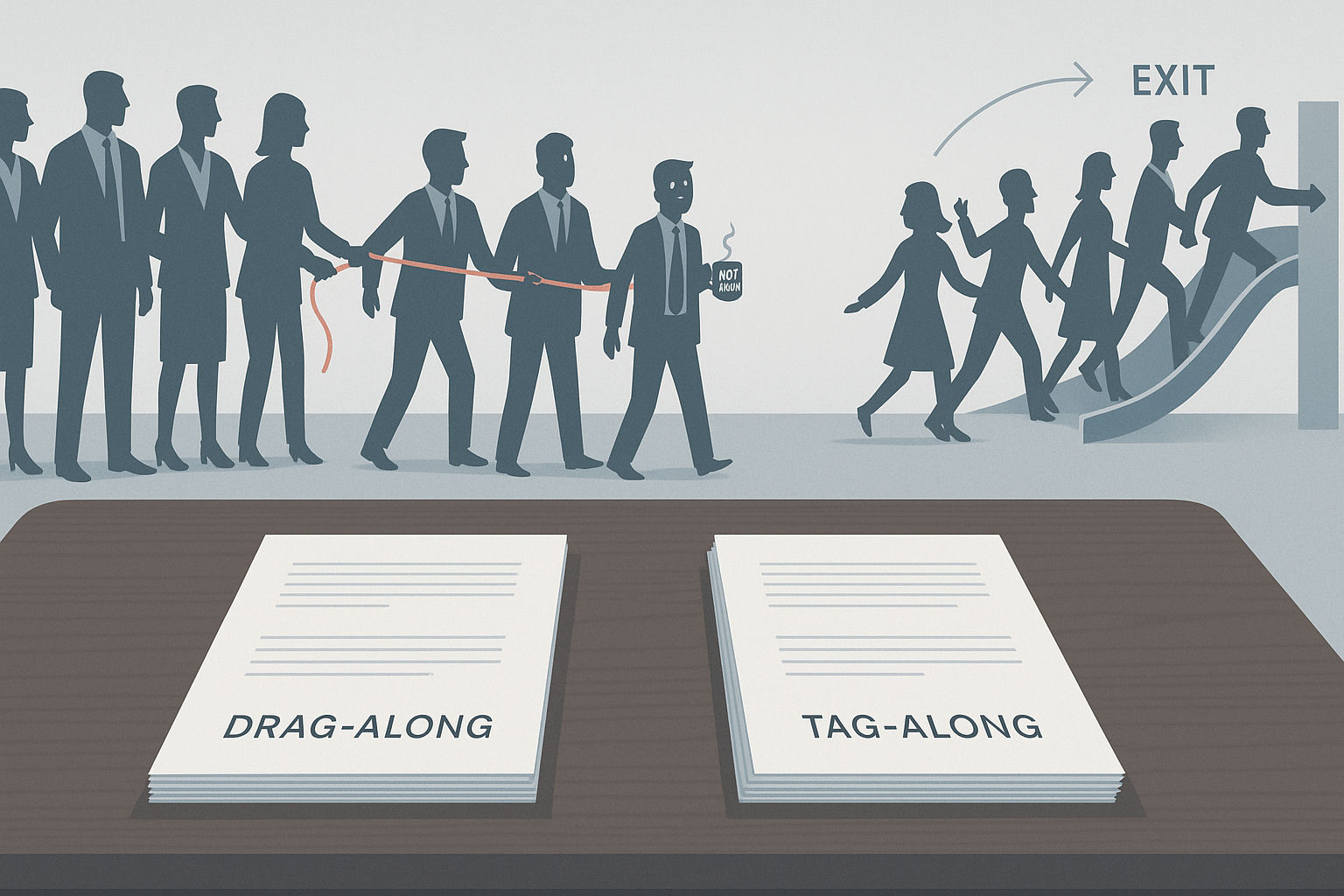

What's the difference between drag-along and tag-along rights?

Drag-along rights allow majority shareholders to force minority shareholders to sell their shares during a company sale, ensuring 100% ownership transfers to the buyer. Tag-along rights work in the opposite direction—they protect minority shareholders by giving them the right to join any sale initiated by majority shareholders on the same terms.

Can minority shareholders block a sale if drag-along rights exist?

No, when drag-along rights are triggered, minority shareholders must sell their shares on the same terms as the majority, whether they like it or not. This prevents small shareholders from blocking valuable acquisition offers or engaging in hold-up behavior to extract special benefits.

What percentage of ownership is typically needed to trigger drag-along rights?

The ownership threshold to trigger drag-along rights typically ranges from 51-75% of shares, depending on how the provision is drafted in your shareholder agreement. This minimum percentage ensures that a true majority controls the decision to sell the company.

How much notice do I get before being dragged into a sale?

Minority shareholders typically receive 15-30 days advance notice before being required to participate in a drag-along sale. During this period, you'll receive formal notice of the pending sale and must prepare to sell on the same terms as the majority shareholders.

Will I get the same price per share as majority shareholders in a drag-along sale?

Yes, drag-along provisions require that minority shareholders receive identical per-share prices and payment terms as the majority shareholders. However, minorities typically only warrant title and capacity to sell, not the broader business warranties that majority shareholders provide to buyers.

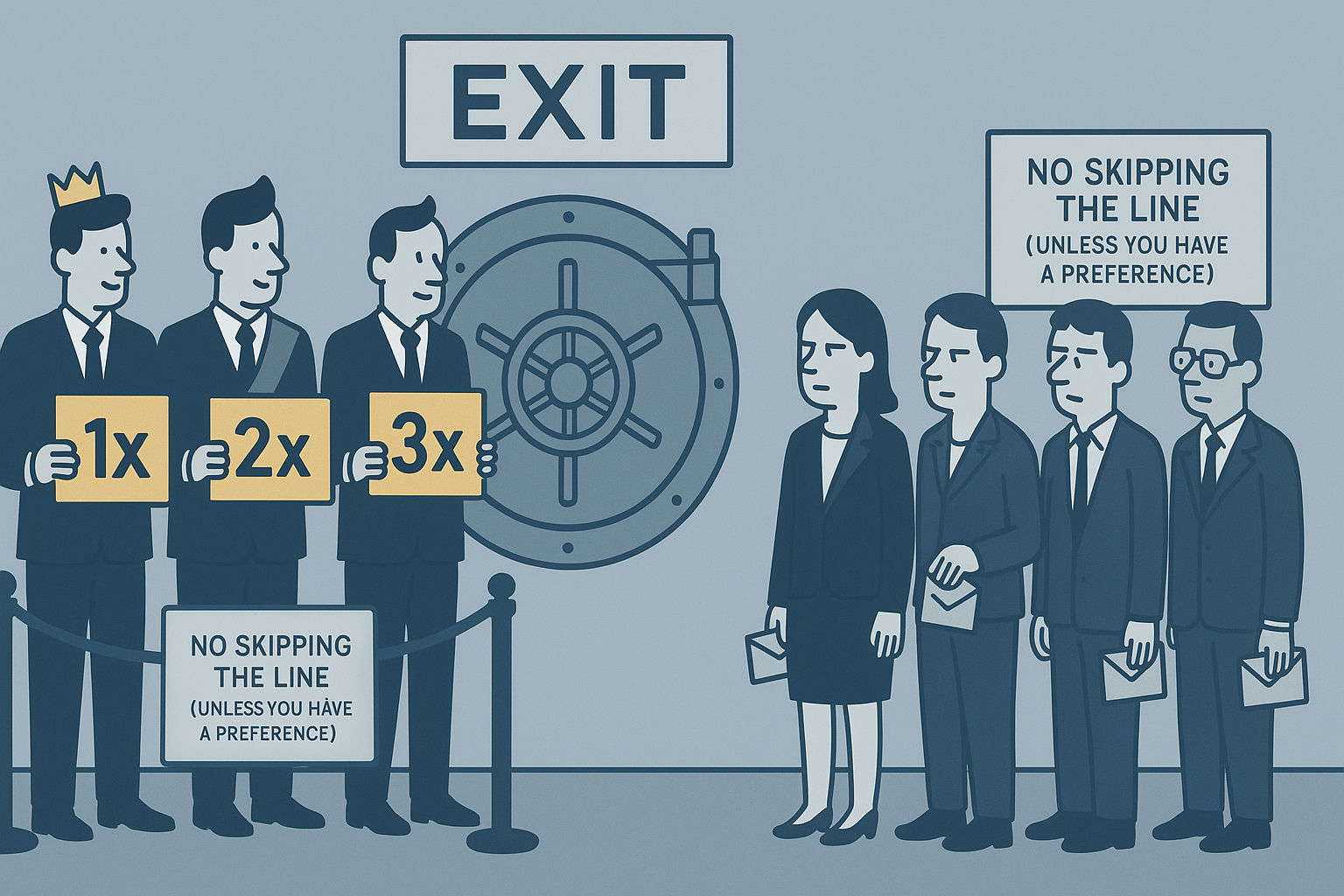

Why do investors insist on drag-along rights in their investment agreements?

Venture capital and private equity investors require drag-along rights to ensure clean exits with 100% ownership transfers, which typically command 20-30% higher valuations than majority-only stakes. These provisions also prevent minority shareholders from blocking sales or demanding disproportionate benefits as conditions for their participation.

Can I be forced to accept non-cash consideration like shares in the acquiring company?

It depends on how your drag-along provision is drafted—specifically the "permitted consideration" clause. Some agreements require cash-only consideration, while others allow non-cash consideration like shares in the acquiring company, so review your shareholder agreement carefully.

What happens if majority shareholders want to sell but I want to exit too?

If you have tag-along rights, you can elect to participate in the sale within the specified response period (typically 10-20 days). The buyer must then purchase your shares on the same terms as the majority's, and the majority's sale becomes conditional on the buyer accepting your shares too.

Do tag-along rights let me sell all my shares or just a portion?

This depends on the "pro-rata participation" clause in your agreement—you may be able to sell all your shares, or only your proportionate amount if the buyer has purchase limits. Well-drafted tag-along provisions specify whether minorities can fully exit or must participate proportionally.

What if the majority wants to sell only part of their stake—can I still tag along?

Yes, but this can create tension between drag-along and tag-along rights. If minorities exercise tag-along rights, it may force the majority to sell more than intended, so well-drafted agreements specify which rights take precedence or how participation is pro-rated in these scenarios.