This article is for startup founders raising venture capital who need to understand how liquidation preferences will affect their payout when they exit.

If you're negotiating a term sheet and wondering whether participating vs non-participating preferences actually matter, or how a 2x multiplier could cost you millions, this guide breaks down exactly how liquidation preferences work, what different terms mean for your exit proceeds, and which questions to ask investors before signing.

Key Takeaways

• Participating preferences let investors get paid twice, receiving their investment back first, then their ownership percentage of remaining proceeds. • Non-participating preferences force investors to choose between their preference amount or converting to common stock, whichever pays more. • Liquidation preference terms can matter more than valuation, a 2x participating preference drastically reduces founder proceeds in modest exits. • Preference multiples above 1x should only appear in rescue financing situations where the company is failing and needs emergency capital. • Always ask explicitly whether preferences are participating or non-participating before signing any term sheet, never assume the terms.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

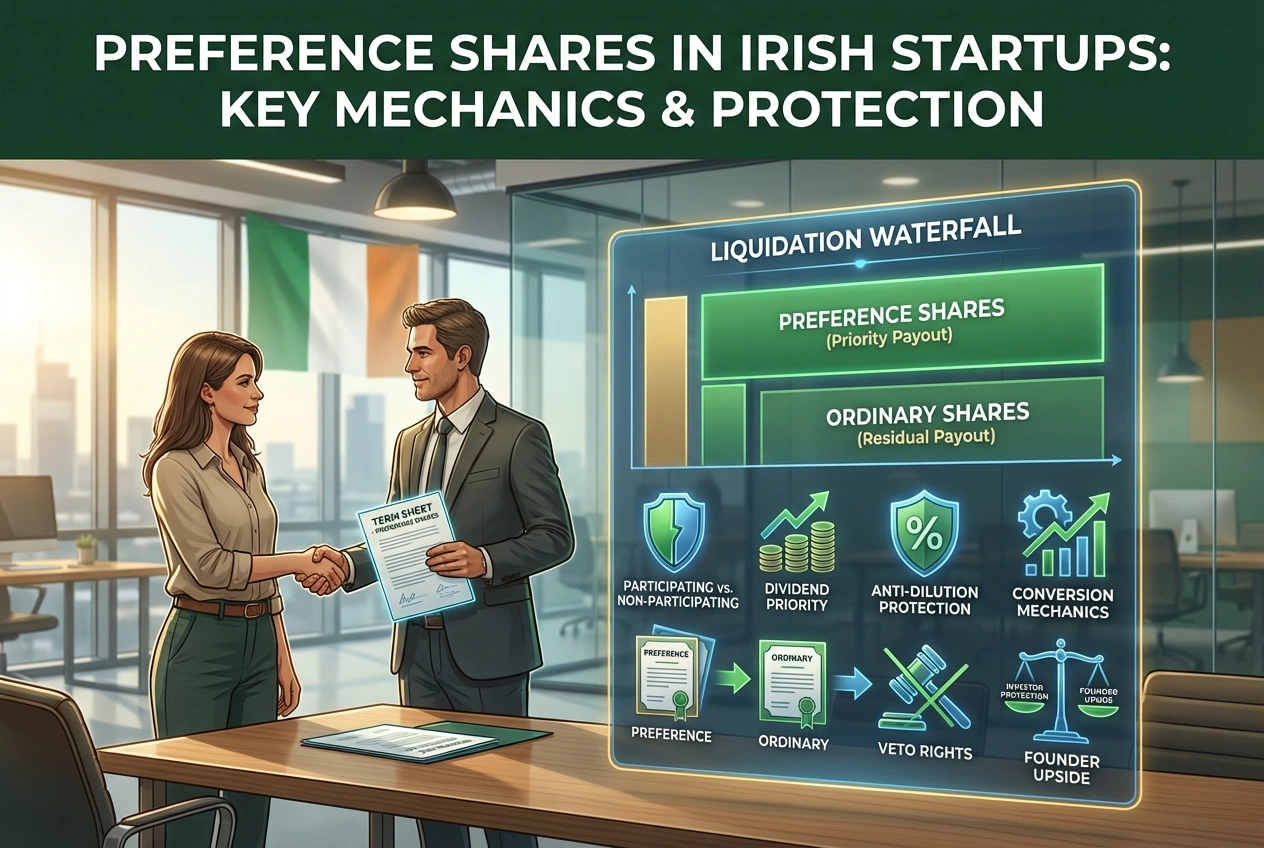

What is a liquidation preference and why do investors get one?

A liquidation preference gives investors the right to receive a specific amount before other shareholders get paid when your company exits through acquisition or liquidation. Investors want this downside protection so they can recover at least their investment before founders profit from the sale, especially if the company sells for less than they paid in.

What's the difference between participating and non-participating liquidation preferences?

With non-participating preferences (standard), investors choose between taking their preference amount OR converting to common stock and taking their ownership percentage, whichever gives them more money. With participating preferences (investor-favorable), investors get paid twice: they receive their preference amount first, then also get their ownership percentage of the remaining proceeds.

How much do I actually receive as a founder if my investor has a 1x participating preference?

Using a typical example: if an investor put in €2M for 20% ownership with 1x participating preference and your company sells for €10M, the investor gets €2M first, then 20% of the remaining €8M (€1.6M), totaling €3.6M. You and other founders would receive the remaining €6.4M (64% of proceeds) despite owning 80% of the company.

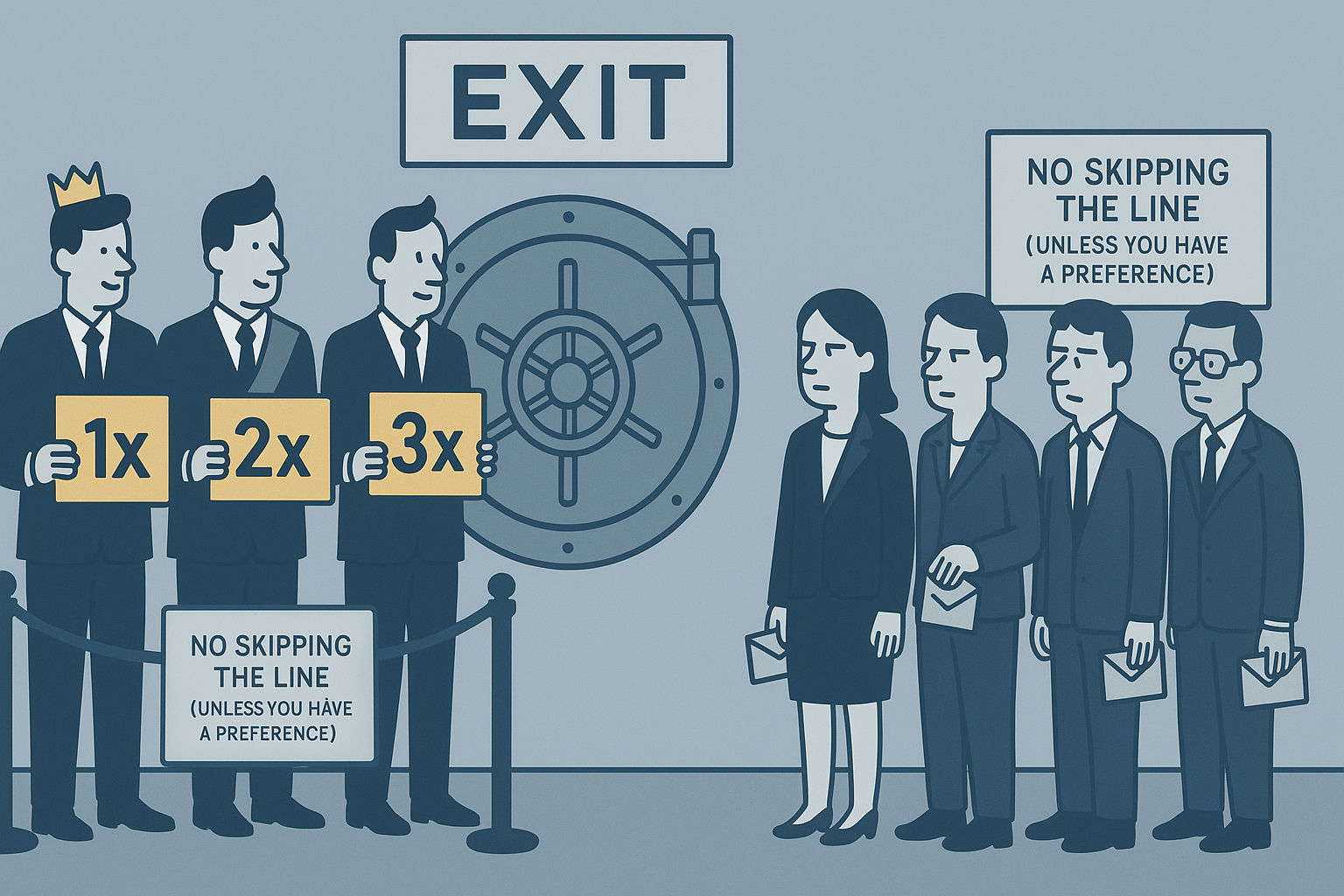

What does a 2x or 3x preference multiple mean for my exit proceeds?

The multiplier determines how many times the investment amount investors receive before anyone else gets paid, so a €2M investment with 2x preference means €4M goes to investors first, and 3x means €6M first. In a €10M exit with 3x participating preference, an investor could receive €6.8M (68% of proceeds) despite only owning 20% of the company, leaving founders with just €3.2M.

Should I accept a higher valuation if it comes with participating preferences or preference multiples?

Not necessarily, liquidation preference terms can matter more than valuation in modest exits. For example, a €10M valuation with 2x participating preference could leave you with €6.67M in a €12M exit, while an €8M valuation with 1x non-participating would give you €9.6M, that's €3M more despite the lower valuation.

When would an investor choose to convert to common stock instead of taking their preference?

With non-participating preferences, investors convert to common stock when their ownership percentage of the total exit proceeds exceeds their preference amount. For example, if an investor has a €2M preference for 20% ownership, they'll convert in any exit above €10M because 20% of a larger number becomes more valuable than the fixed €2M preference.

Are preference multiples above 1x ever acceptable?

Multiple preferences (2x, 3x) should only appear in rescue financing situations where the company is failing and investors are taking extraordinary risk to keep it alive. Anything above 1x requires strong justification based on extraordinary circumstances, it's not standard for healthy funding rounds.

What questions should I ask before signing a term sheet with liquidation preferences?

Get explicit written confirmation on four key points: Is this participating or non-participating? What's the preference multiple (anything above 1x needs justification)? How does this rank relative to other investors if there are multiple preference layers? At what exit value does conversion make sense for the investor (calculate the break-even point)?

.webp)

%20(1).webp)