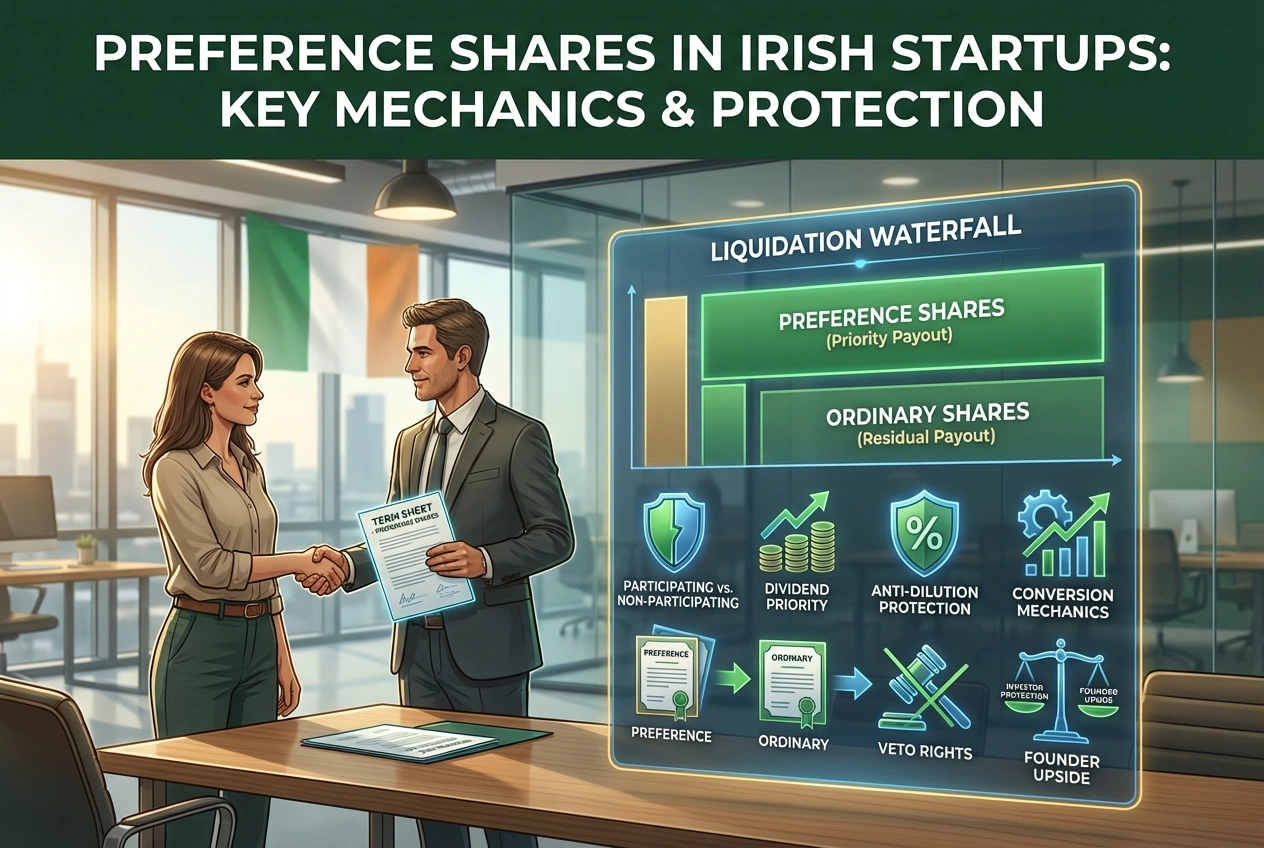

Preference Shares Explained: Types and Rights for Irish Startups

When an institutional investor (such as a VC) puts money into your startup, they rarely take ordinary shares . In almost every priced funding round , investors receive preference shares, a separate class of share that comes with rights ordinary shareholders do not have. Understanding what those rights are, and how they affect you as a founder, is essential before you sign a term sheet .

This guide explains how preference shares work, the different types you will encounter, the specific rights attached to them, and what founders need to watch for when negotiating preference share terms.

What Are Preference Shares?

Preference shares are a class of share that carries preferential rights over ordinary shares. The preference typically relates to dividends , return of capital (funds money received on a liquidation or exit), or both.

Under the Companies Act 2014, an Irish company can create different classes of shares with different rights attached. There is no statutory definition of "preference share", the rights are defined entirely by the company's constitution and the terms agreed between the company and the investor.

In the startup context, preference shares are the standard instrument used in priced equity rounds. When a VC, or sometimes an angel investor, leads a Seed, Series A, or later round, they will almost always subscribe for a new class of preference shares rather than ordinary shares. This gives them downside protection while still allowing them to participate in the upside if the company succeeds.

Founders and early employees, by contrast, typically hold ordinary shares (or sometimes non-voting B ordinary shares for employees, advisors etc.). The interaction between these two classes, particularly on an exit, is one of the most important dynamics in your company's share capital structure.

Types of Preference Shares

Not all preference shares are the same. The specific rights attached depend on what is negotiated in the term sheet and documented in the shareholders' agreement and constitution. Here are the main types you will encounter:

Participating vs Non-Participating

This is the most consequential distinction for founders.

Non-participating preference shares give the investor a choice on exit: take their liquidation preference (typically 1x their investment back) or convert to ordinary shares and take their pro-rata share of the total proceeds. They choose whichever option gives a higher return. This is the standard in most founder-friendly deals.

Participating preference shares give the investor their liquidation preference back and a pro-rata share of the remaining proceeds as if they had converted to ordinary. This is sometimes called "double-dipping" because the investor effectively gets paid twice, once from the preference and once from the equity upside. Participating preferences are less common in early-stage Irish deals but can appear in later rounds or in deals led by more aggressive investors.

Cumulative vs Non-Cumulative

This relates to dividend rights.

Cumulative preference shares accrue a dividend whether or not the company declares one. If the company does not pay the dividend in a given year, it rolls over and accumulates. The accumulated amount must be paid before any dividend is paid to ordinary shareholders.

Non-cumulative preference shares carry a dividend right, but if the company does not declare a dividend in a given year, the entitlement for that year lapses. In practice, most Irish startup preference shares are non-cumulative because early-stage companies rarely pay dividends.

Redeemable Preference Shares

Redeemable shares can be bought back by the company at a future date, either at the company's option or the shareholder's option. Under the Companies Act 2014, a company can issue redeemable shares provided its constitution authorises it and the redemption is funded from distributable profits or the proceeds of a new share issue.

Redeemable preference shares are sometimes used in structured exits or where an investor wants a defined return timeline. They are more common in private equity transactions than in venture capital rounds.

Convertible Preference Shares

Convertible preference shares can be converted into ordinary shares, either at the holder's election or automatically upon certain trigger events. This is the most common type in Irish startup fundraising, virtually all VC preference shares are convertible. This allows the preference shareholder to convert them into ordinary shares for whatever reason (e.g. the ordinary shares would receive more on an exit or to avail of voting rights).

Rights Attached to Preference Shares

The value of preference shares lies in the specific rights attached to them. These are negotiated as part of the funding round and documented primarily in the company's constitution , and may also be contained in the shareholders' agreement, and the subscription agreement.

Dividend Priority

Preference shareholders may have the right to receive a dividend before any dividend is paid to ordinary shareholders. For Irish startups, this usually dividend accrues but is rarely actually paid out. The accrued dividend becomes relevant on exit, where it is added to the liquidation preference amount.

Liquidation Preference

This is the most important economic right for investors. A liquidation preference entitles the preference shareholder to receive a specified amount before any proceeds are distributed to ordinary shareholders.

The standard is a 1x non-participating liquidation preference, meaning the investor gets their original investment amount back first. If the exit proceeds exceed the total liquidation preferences, the investor can choose to convert to ordinary and share the exit proceeds pro-rata instead.

Higher multiples (1.5x, 2x) and participating structures shift more value to the investor at the expense of founders and ordinary shareholders. Understanding the equity dilution impact of different preference structures is critical before agreeing terms. Depending on the liquidation preference, and the proceeds received as part of a sale of the company, the preference shareholders may receive all of the proceeds, with none remaining for the ordinary shareholders, including the founders and the key employees that built the startup from the beginning.

Voting Rights

Preference shareholders may have limited, full, or no voting rights on ordinary company matters. However, they almost always have consent rights (also called protective provisions, reserved matters , or veto rights) on specific matters, such as issuing new shares, changing the constitution, taking on debt above a threshold, or selling the company. Consent rights are a right granted to certain investors (usually lead or substantial investors) contained in the shareholders' agreement, rather than a right attaching to the preference shares.

These consent rights give investors significant influence over key decisions even if they hold a minority of the total shares.

Anti-Dilution Protections

Most preference share terms include anti-dilution provisions that adjust the conversion ratio if the company later issues shares at a lower price (a down round). The two main mechanisms are:

Broad-based weighted average - The conversion price is adjusted based on a formula that takes into account the size of the down round relative to the company's total capitalisation. This is the market standard in Irish venture deals.Full ratchet - The conversion price is reduced to the new, lower price regardless of the size of the down round. This is punitive for founders and uncommon in early-stage deals.

Conversion Mechanics

Convertible preference shares can be converted into ordinary shares under specific circumstances. The conversion terms determine when and how this happens.

Optional Conversion

The investor can choose to convert their preference shares into ordinary shares at any time. This is useful when the ordinary shares are worth more than the liquidation preference, for example, on a high-value exit where converting and taking a pro-rata share produces a better return than taking the preference amount.

Automatic Conversion

Preference shares typically convert automatically on certain trigger events:

Qualifying IPO - If the company lists on a recognised stock exchange at or above a specified valuation, all preference shares convert to ordinary. The IPO threshold is negotiated in the term sheet.Majority consent - If a specified majority of preference shareholders (often 75%) vote to convert, all preference shares in that class convert. This prevents a small minority from blocking a conversion that benefits the majority.

Conversion Ratio

The conversion ratio determines how many ordinary shares each preference share converts into. Initially, this is usually 1:1. However, anti-dilution adjustments can change this ratio, resulting in the investor receiving more ordinary shares per preference share on conversion.

What Happens to Preference Rights on Conversion

Once preference shares are converted to ordinary shares, all preferential rights, liquidation preference, dividend priority, consent rights, are extinguished. The converted shares rank equally with all other ordinary shares. This is why investors only convert when the ordinary share value exceeds their preference entitlement.

How Preference Shares Affect Founders

Preference shares are not just a technical detail, they directly affect how much money you take home on an exit and how much control you retain while running the company.

Waterfall Analysis

On any exit (trade sale, IPO, or liquidation), proceeds are distributed according to a "waterfall", a priority order that pays preference shareholders before ordinary shareholders. If you have multiple rounds of preference shares (Series A, B, C), the waterfall can become complex, with each class having different preference amounts and seniority.

Running a waterfall analysis at different exit valuations shows you exactly what founders and employees receive after investor preferences are satisfied. This is essential before accepting a term sheet, a headline valuation can look attractive while the preference stack leaves little for ordinary shareholders at moderate exit values.

Board Composition and Veto Powers

Investors with preference shares often negotiate board seats and veto rights over major decisions. While this is separate from the share rights themselves, the two are closely linked, the same negotiation that sets the preference terms also sets the governance structure.

Founders should understand that issuing preference shares is not just about economics. It is about governance, control, and the practical ability to run the company without needing investor approval for every significant decision.

Negotiating Preference Terms

The most founder-friendly structure is a 1x non-participating liquidation preference with broad-based weighted average anti-dilution and standard protective provisions . This is the market norm for early-stage Irish deals.

Watch out for:

Participating preferences - They significantly reduce founder returns on moderate exits.High liquidation multiples (1.5x or above) - They increase the threshold at which ordinary shareholders start to benefit.Full ratchet anti-dilution - It punishes founders disproportionately in a down round.Cumulative dividends - They add to the preference stack over time, compounding the waterfall effect.

Creating Preference Shares in an Irish LTD

If your company currently has only ordinary shares (which is the case for most newly incorporated Irish LTDs), creating a new class of preference shares requires several steps.

Constitutional Amendments

The company's constitution must authorise the creation of the new share class. For a company incorporated under the Companies Act 2014 as an LTD, this typically requires a special resolution (75% of votes cast) to amend the constitution to include the rights attaching to the new class.

Shareholder Resolutions

The directors need authority to allot shares . Under Section 69 of the Companies Act 2014, the directors of an LTD have a general authority to allot shares unless the constitution restricts it. If the constitution does restrict allotment, a shareholders' resolution is required.

Existing shareholders also have statutory pre-emption rights under Section 69, meaning new shares must first be offered to them in proportion to their existing holdings. In a funding round, pre-emption rights are typically disapplied by special resolution to allow the new shares to be issued directly to the incoming investors.

CRO Filings

After issuing the preference shares, the company must file a Form B5 (return of allotments) with the Companies Registration Office within 30 days. The form records the number, nominal value, and class of shares allotted.

Documenting Rights

The rights attaching to preference shares should be documented in:

The company's constitution (amended articles) - This is the primary legal document that defines the share class rights.

The shareholders' agreement - This typically contains additional detail on investor protections, consent rights, and governance arrangements that go beyond what is in the constitution.

The subscription agreement - This records the specific terms of the investment, including the subscription price, warranties , and conditions precedent .

Ensuring consistency across all three documents is critical. Discrepancies between the constitution and the shareholders' agreement are a common source of disputes in later rounds or on exit.

Key Takeaways

Preference shares give investors priority over ordinary shareholders on dividends and return of capital, in exchange for limited voting rights on day-to-day matters.

The most common structure in Irish startup deals is 1x non-participating convertible preference shares with broad-based weighted average anti-dilution.

Participating preferences and high liquidation multiples significantly reduce what founders receive on exit, run a waterfall analysis before agreeing terms.

Creating a new share class requires amending the constitution, disapplying pre-emption rights, and filing with the CRO.

Preference share rights should be documented consistently across the constitution, shareholders' agreement, and subscription agreement.

This article is for informational purposes only and does not constitute legal or financial advice. Consult a qualified professional before making decisions about share structures or fundraising.

.webp)