This article is aimed at Irish company founders, CEOs, CFOs, and corporate legal counsel who are considering or need to carry out a share capital redenomination, especially when dealing with foreign investors or multinational group structures.

After reading, you will understand what redenomination entails, when it’s appropriate, the required shareholder approvals and class consents, how to calculate conversion rates and handle rounding, and the specific CRO filing deadlines and documentation needed to execute the change correctly.

Key Takeaways

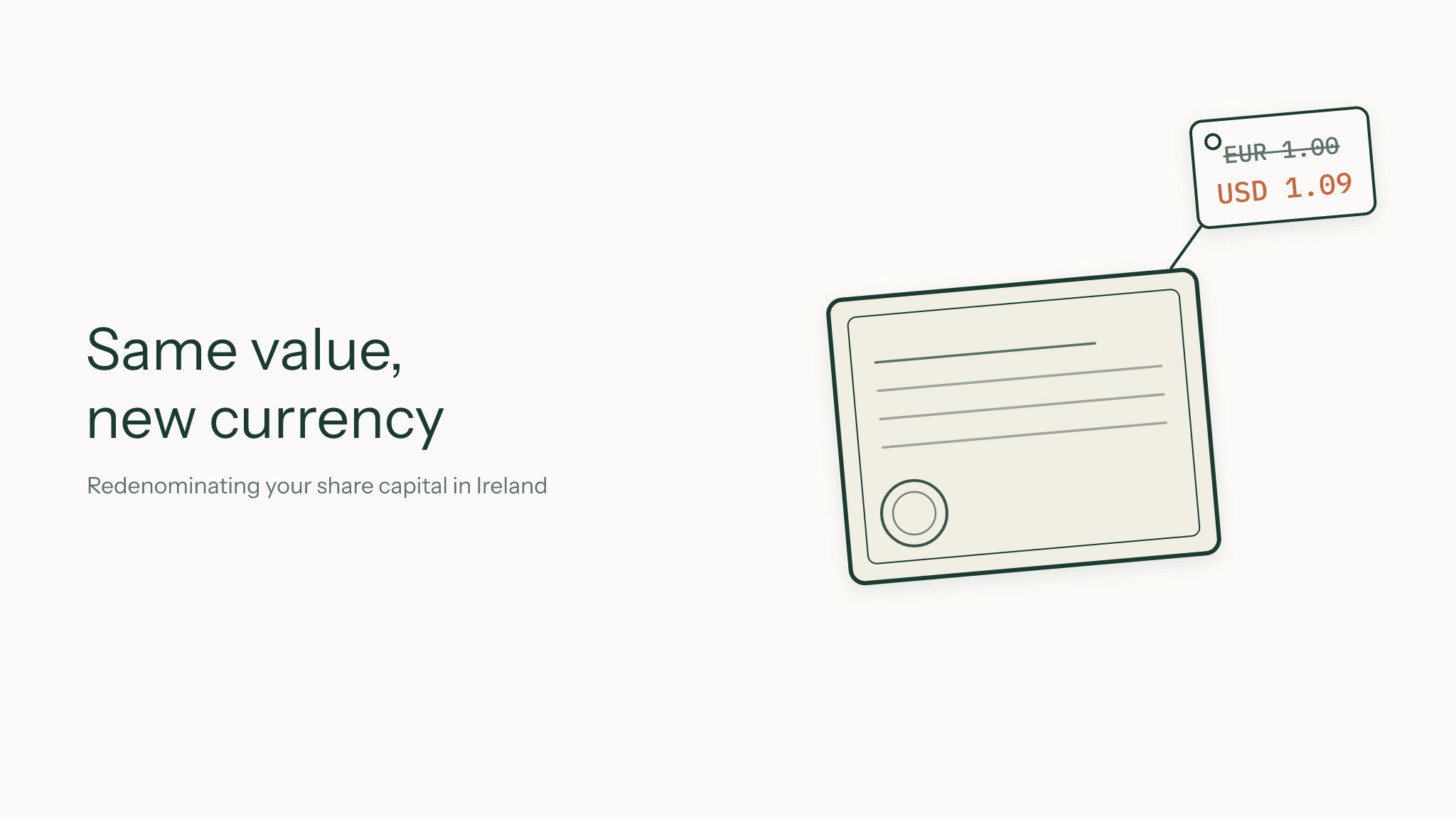

Redenominating share capital changes the currency of shares without altering ownership percentages or moving money.

A special resolution (75% majority) and, where applicable, class consents are required to approve the redenomination.

The conversion must fix a specific date and published rate, and rounding rules must be consistently applied to avoid inconsistencies.

All filings, including Form G1 for the special resolution and Form B7 for capital variation, must be submitted to the CRO within the statutory deadlines (15 days for the resolution, one month for capital variation).

Common mistakes include unclear conversion dates or rates, inconsistent rounding, ignoring class rights, and missing CRO filing deadlines.

Laura Ryan is a practising Barrister at the Bar of Ireland. She graduated from the Honourable Society of King’s Inns in 2024, having previously qualified and practised as a Chartered Accountant in a big four accounting firm.

Redenominating share capital means re‑expressing existing shares in a different currency without changing ownership or percentages. It relabels the nominal value of each share from one currency to another, leaving the same money expressed in a new unit. The underlying share count and each holder’s percentage remain unchanged.

Why do companies choose to redenominate their share capital?

Companies redenominate share capital to match investor, group, or revenue currency, simplifying fundraising and consolidation. A US or international investor round often drives the change, as investors model cap tables in dollars. Aligning capital with the currency earned or spent also reduces accounting friction and future fundraising complexity.

How are the approvals and resolutions obtained for a redenomination?

A redenomination requires shareholder authority, often a special resolution with at least a 75% majority, because it amends the constitution. Class consents are needed when multiple share classes are affected, requiring written consent from holders of 75% nominal value or a separate class special resolution.

What are the key steps in the currency conversion process?

The conversion hinges on fixing a conversion date and a published rate in the resolution. The chosen rate is applied to each share’s nominal value, and the company decides how to handle resulting fractions through rounding rules, ensuring the number of shares and ownership percentages stay unchanged.

What filings are required after a redenomination?

After resolutions pass, companies must file a special resolution and amended constitution on Form G1 to the CRO within 15 days, and if capital variation applies, file Form B7 within one month. Additionally, update the register of members, re‑issue share certificates, and reconcile the cap table promptly.

%20(1).webp)