Founders and directors of Irish limited companies who track performance day-to-day and need to comply with statutory reporting requirements.

Readers will learn why statutory accounts must use accruals, how cash and accruals views differ, and what monthly routine best balances both perspectives.

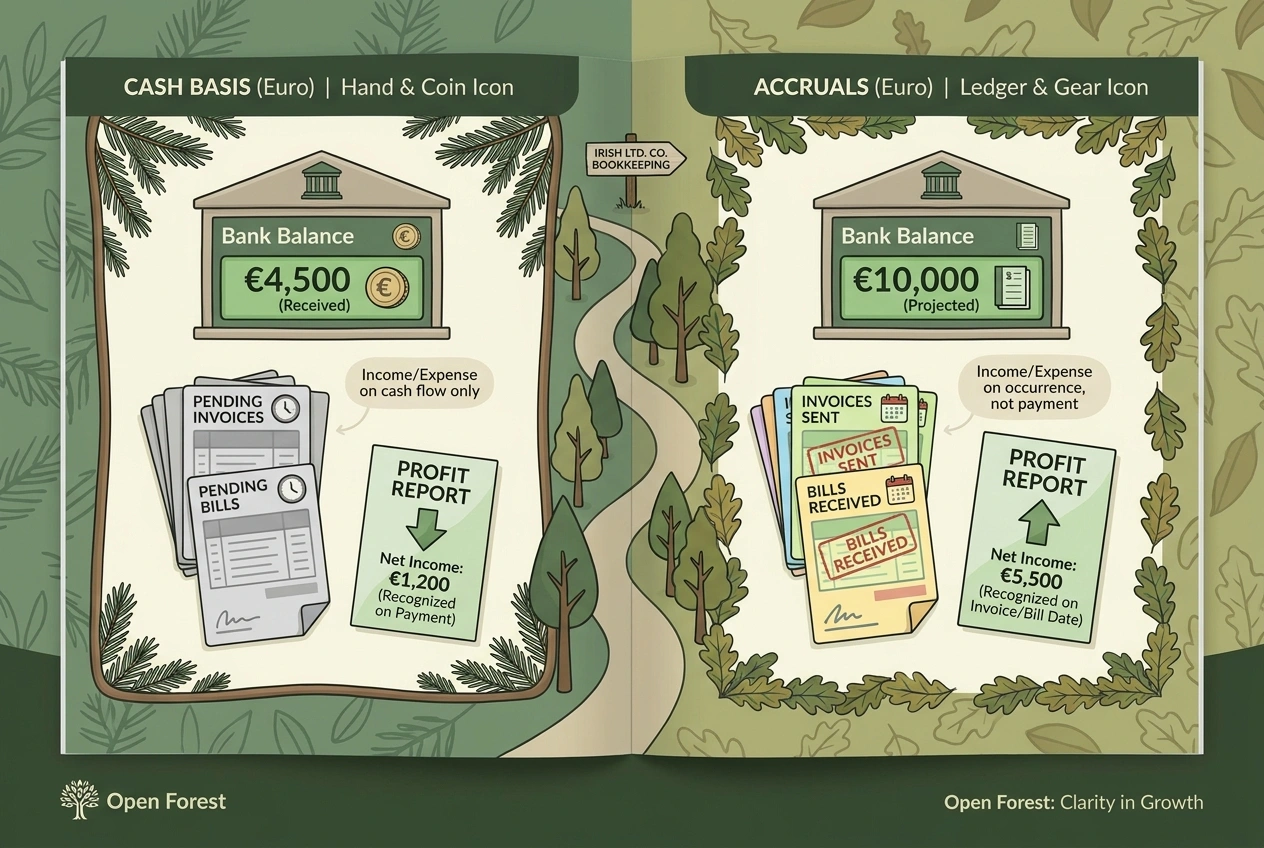

Cash basis vs accruals Ireland is a practical question for founders because the method you use changes when income, costs and profit appear in your books.

Cash basis bookkeeping follows the money. Accruals bookkeeping follows the economic activity. Both views are useful, but they do not serve the same purpose. For Irish limited companies, the key point is that statutory accounts are prepared on an accruals basis, even if founders also track cash closely day to day.

What is cash basis bookkeeping?

Cash basis bookkeeping records income when money is received and costs when money is paid.

It is simple to understand because it follows the bank account. If a customer pays today, income appears today. If you pay a supplier tomorrow, the cost appears tomorrow. Many founders default to this view because it matches how they think about cash flow .

Cash basis can be useful for:

Short-term cash monitoring

Simple owner-managed businesses

Early-stage founder dashboards

Understanding whether the bank balance can cover bills

Its weakness is timing. A company can complete work in May, invoice in June and get paid in July. Under a cash view, the income appears in July, even though the work happened earlier. That can distort monthly performance.

Cash basis also struggles where the company has unpaid invoices, supplier bills , stock, loans, VAT or payroll liabilities.

What is accruals bookkeeping?

Accruals bookkeeping records income when it is earned and costs when they are incurred, regardless of payment timing.

This gives a more accurate view of business performance. If you deliver a service in May, the income belongs in May even if the customer pays later. If you receive a supplier service in May, the cost belongs in May even if the bill is paid in June.

Accruals bookkeeping uses concepts such as:

Debtors, for amounts customers owe you

Creditors, for bills you owe suppliers

Accruals, for costs incurred but not yet invoiced

Prepayments, for costs paid in advance

Deferred income, for cash received before work is delivered

The glossary entry on accruals is useful if you want the accounting term in plain English.

Author's tip: Accruals are not just accountant adjustments. They help founders see whether the business model is profitable before cash timing hides the answer.

Accruals also fit naturally with double-entry bookkeeping , where every transaction affects at least two accounts.

Which method should an Irish LTD use?

An Irish limited company should keep books capable of supporting accruals-based financial statements .

The Companies Act 2014 requires companies to keep adequate accounting records and prepare financial statements that give a true and fair view. In practice, most Irish LTDs prepare accounts under FRS 102, which is built on accruals principles.

Cash basis can still appear in limited ways. Founders may use cash dashboards internally. VAT can sometimes be accounted for on a moneys received basis where Revenue conditions are met. Sole traders may have different tax accounting considerations. But for an Irish limited company, statutory reporting points back to accruals.

The practical reality is that some companies run a cash-like system during the year and the accountant makes accruals adjustments at year end. That can work for very small companies , but it often creates surprises. Profit changes late, unpaid bills appear suddenly and directors do not see the real performance until after the year has closed.

Clean accruals bookkeeping reduces those surprises.

How does the method affect VAT?

VAT has its own timing rules, so the bookkeeping method must align with the VAT basis your company uses.

Revenue describes two VAT accounting methods: invoice basis and moneys received basis. Under the invoice basis, VAT is generally accounted for when the invoice is issued. Under the moneys received basis, VAT is generally accounted for when payment is received, where the trader is eligible.

This is not the same as saying the whole company can prepare statutory accounts on a cash basis. VAT timing is a specific tax reporting issue.

The impact on cash flow can be significant. On the invoice basis, a company may owe VAT before a customer has paid. On the moneys received basis, VAT may follow customer receipts, which can help cash flow where allowed.

If VAT is relevant, read our guide to Value Added Tax for new Irish companies and make sure your accounting software is set up for the correct basis.

We have seen founders caught out by the invoice basis more than once. A common pattern: a large invoice is raised in the last month of a VAT period, the customer does not pay for 60 days, but the VAT is due to Revenue on the return date. If your company regularly invoices before payment, check whether the moneys received basis would be available and beneficial.

How does the method affect Corporation Tax and profit?

Accruals can show profit before cash is received, while cash tracking can show pressure before profit disappears.

That sounds contradictory, but both views can be true. A company may be profitable on an accruals basis because it has delivered work and issued invoices. It may still run out of cash if customers pay late, VAT is due, payroll lands or loan repayments fall due.

This is why founders should not rely on either profit or bank balance alone.

A proper management view should include:

Profit and loss on an accruals basis

Balance sheet with debtors and creditors

Cash-flow forecast

VAT and payroll liabilities

Aged receivables and payables

Corporation Tax is also based on accounting profit adjusted for tax rules, not simply the bank balance. That is why accruals bookkeeping supports stronger tax compliance .

In practice, this means: Your company can show a profit and still have a cash problem. The fix is not to ignore accruals. It is to track cash alongside accruals.

What hybrid approach works best for founders?

The best practical approach is accruals bookkeeping with a separate cash-flow view.

This gives you reliable accounts and a founder-friendly view of the bank position . You do not have to choose between compliance and cash awareness.

A good monthly routine is:

Post sales invoices and supplier bills when issued or received

Reconcile bank and card accounts

Review debtors and creditors

Post accruals or prepayments where material

Check VAT and payroll liabilities

Update a short cash-flow forecast

A financial model can sit beside the books, but it should not replace them. The model looks forward. The bookkeeping record shows what has actually happened.

This approach also makes annual accounts easier because the records already reflect the right accounting basis.

Need help choosing the right bookkeeping setup?

What to do next

For an Irish limited company, accruals should be the foundation of the books. Cash tracking should sit alongside it, not replace it.

If you are still managing the company from the bank balance, start by adding unpaid customer invoices, supplier bills, VAT liabilities and payroll costs into your monthly review. Open Forest can help you build a bookkeeping routine that supports both compliance and better founder decisions.