Irish founders, startup boards and HR leads who are responsible for designing equity compensation plans for employees and advisors.

Readers will understand the key differences, documentation requirements, tax implications and specific situations where a direct share award is the better choice over traditional share options.

Key Takeaways

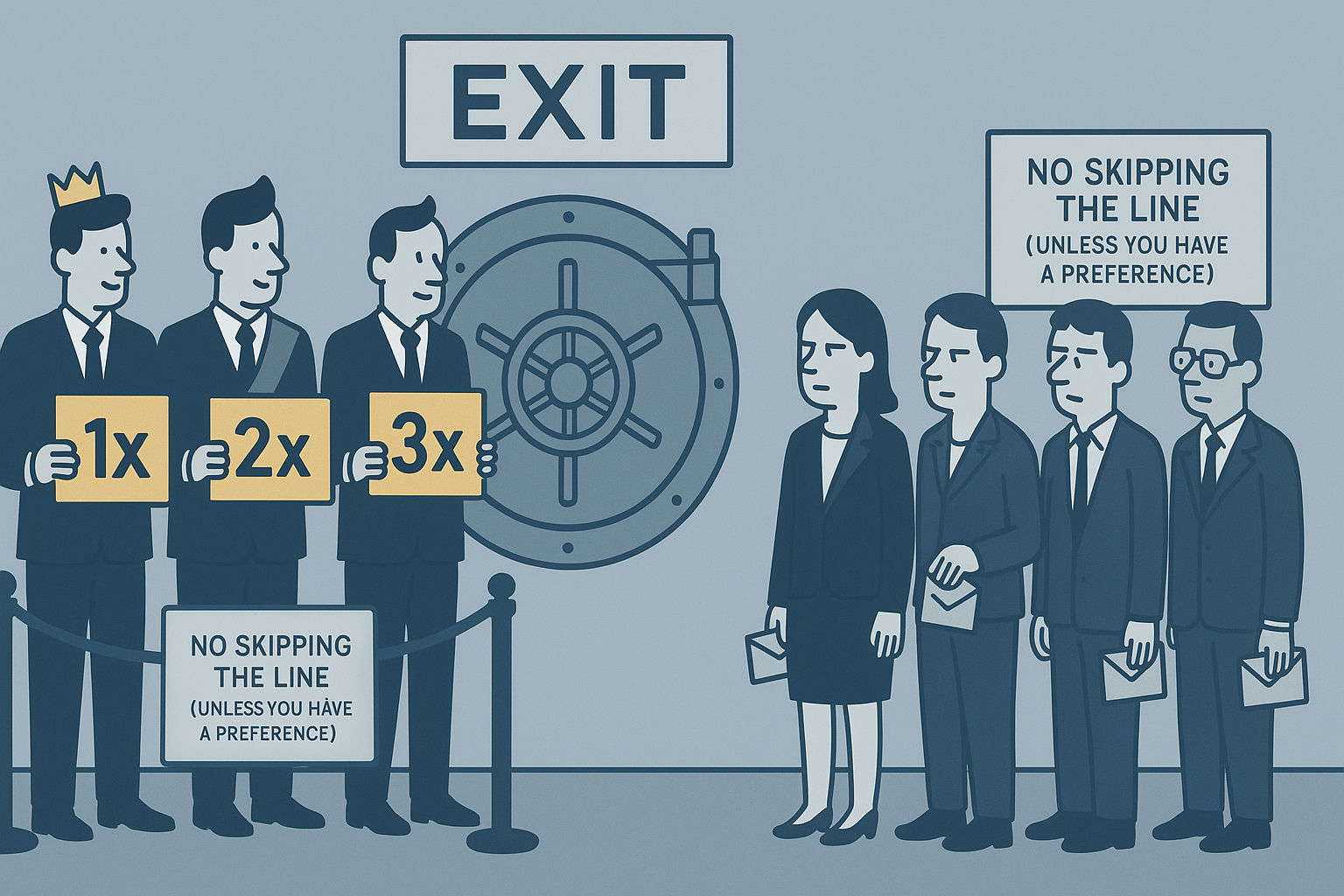

Direct share awards give immediate ownership and shareholder rights but trigger immediate tax and dilution.

They simplify long-term administration by eliminating exercise events and expiry tracking compared to options.

Reverse vesting through leaver provisions can replicate the retention effect of options without an exercise step.

Most suitable for founders, very senior hires and advisors; options remain preferable for most early employees.

A direct share award is an issue or transfer of shares to an employee with no exercise step, making the recipient a shareholder immediately with rights subject to any restrictions in the articles or shareholders agreement.

How does a direct share award differ from an option grant?

Direct awards provide immediate ownership without an exercise cost or decision later, while options defer ownership and allow the recipient to decide if paying market value is worthwhile in the future.

When should Irish startups use direct share awards?

They suit founder top-ups, strategic senior hires wanting immediate ownership, advisor awards where alignment matters, and investor-driven requests for a key executive on the register.

How is vesting handled with direct share awards?

Reverse vesting uses leaver provisions and compulsory transfer rules so the company can buy back shares at a low price if the employee leaves early, achieving retention similar to option vesting.